The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month.

Beta = 0.75

R-square = 0.65

Standard Deviation of Residuals = 0.06 (i.e., 6% monthly)

Assuming that monthly returns are approximately normally distributed, what is theprobability that this market-neutral strategy will lose money over the next month?

Assume the risk-free rate is .5% per month.

Answer:

0.33853

Explanation:

Given that, the expected rate of return of the market-neutral position is equal to the risk-free rate plus the alpha:

0.5%+ 2.0% = 2.5%

Hence, since we assume that monthly returns are approximately normally distributed.

The z-value for a rate of return of zero is

−2.5%/6.0% = −0.4167

Therefore, the probability of a negative return is N(−0.4167) = 0.33853

Answer:

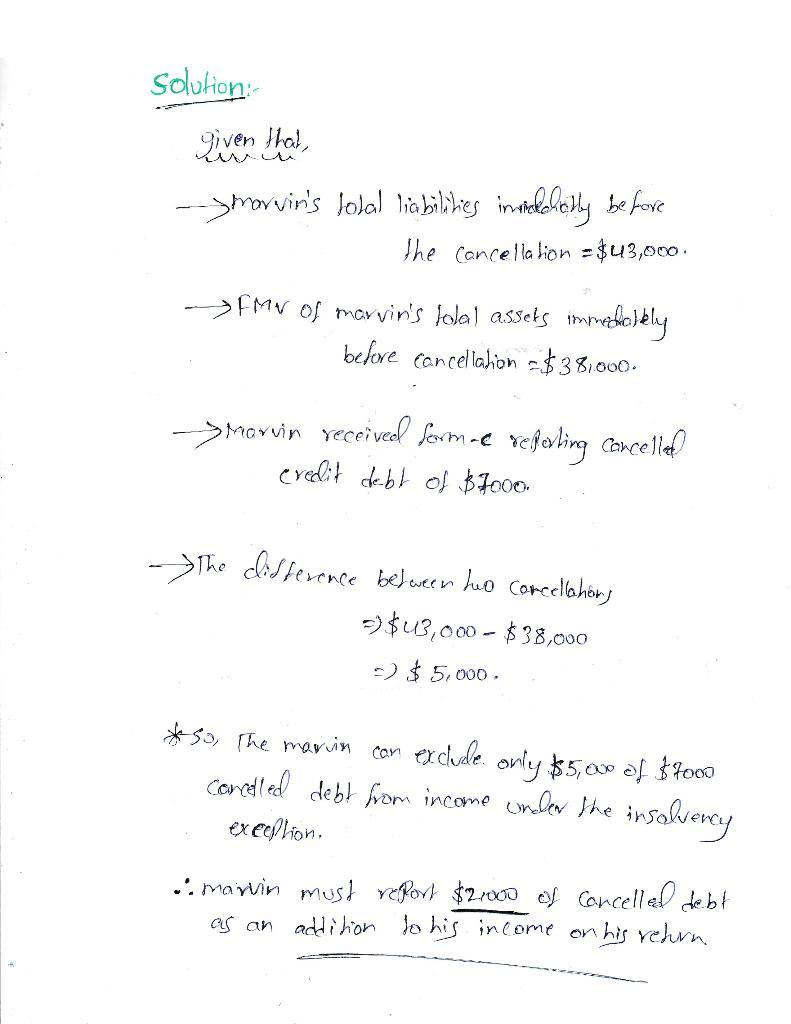

$2000 of canceled debt that Marvin must report on his return

Explanation:

Please see attachment

The three out of four in the choices is classified as a selling expense such as sales salaries, delivery expense, and advertising expense. This three are under the account of selling expense while the Cost of good sold or for short COGS is also classified as an expense but the cogs we sold needs to be matched <span>with the pertinent sales on the </span>income<span> statement.</span>

Answer:

Option C

Explanation:

It is given that the Hillary has received the check of $ 5,000 on the last week of the December.

Therefore,

Under constructive receipt she is taxed on income at the time the check is received or made available to Hillary i.e on the last year.

Thus, She will be taxed on $ 5000 for the last year

Hence, the correct answer is option (C)

<span>c. make more money hope it helped </span>