Answer:

a) $3

b) $2

c) 1449

Explanation:

Given:

The cost for a carton of milk = $3

Selling price for a carton of milk = $5

Salvage value = $0 [since When the milk expires, it is thrown out ]3

Mean of historical monthly demand = 1,500

Standard deviation = 200

Now,

a) cost of overstocking = Cost for a carton of milk - Salvage value

= $3 - $0

= $3

cost of under-stocking = Selling price - cost for a carton of milk

= $5 - $3

= $2

b) critical ratio =

or

critical ratio =

or

critical ratio = 0.4

c) optimal quantity of milk cartons = Mean + ( z × standard deviation )

here, z is the z-score for the critical ration of 0.4

we know

z-score(0.4) = -0.253

thus,

optimal quantity of milk cartons = 1,500 + ( -0.253 × 200 )

= 1500 - 50.6

= 1449.4 ≈ 1449 units

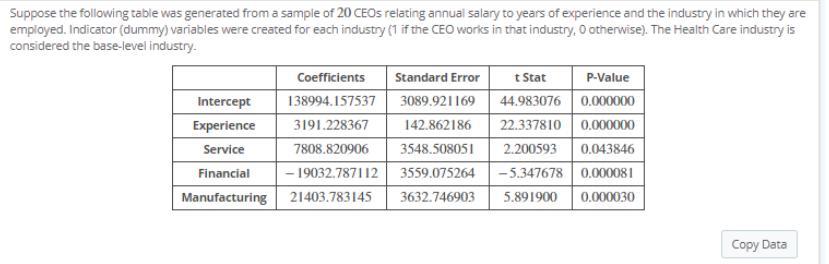

Answer: $19,032.79

Explanation:

There is some data missing that I was unable to find so I will answer a similar question and can use your data to answer this using mine as a reference.

Because the healthcare industry is the base industry, the estimated difference in the annual salary is:

= 0 - Coefficient of Financial industry

= 0 - (-19,032.787112)

= 0 + 19,032.787112

= $19,032.79

Answer:

If the asset’s book value exceeds the proceeds received from disposal by sale, the company records a gain.

Explanation:

All of the other options are true except for this option;

If the asset’s book value exceeds the proceeds received from disposal by sale, the company records a gain.

It is expected that the company should record a loss rather.

Hence, If the sales of a plant asset exceeds its book value, the company records a gain.

Answer:

The answer is B, C, and E.

Explanation:

Saw this post and one other neither had the correct answer so i figured i would help anyone out that needs the correct answer.