<span>The movement of storage of materials into a firm is material management. This is a technique that concerns itself with organizing, planning, and controlling how and what materials flow from the time they are originally purchased until they reach their destination.</span>

Answer:

Me I would find out everything I need to know I would check to see what’s there Star are see how many complain and how long they been open ETC

Explanation:

Answer:

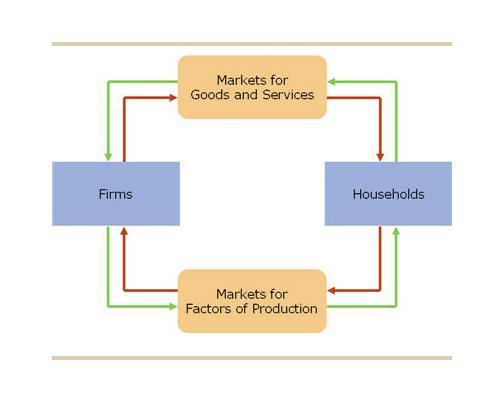

production.

Explanation:

Based on this model, households earn income when firms purchase resources from them. Households own labor (individuals' work) and capital (savings and investments) resources.

Firms earn income when households purchase goods and services from them.

In forex trading When someone is holding a long position in a foreign currency, then the person can hedge with a short position in a currency forward contract.

What do we mean by long position in a foreign currency?

Long can be explained as when someone buy with the expectation that the purchase will rise in term of value in the future.

At a long on a currency, one is try to bet the base currency, that it will strengthen compared with the quote currency.

Learn more about foreign currency here;

brainly.com/question/11160294