Answer:

Answer is option C, ALTERING SITUATIONAL FACTORS AND MAKING IT DIFFICULT TO PRACTICE WASTEFUL BEHAVIOUR.

Explanation:

Employee behaviour is defined as an employee’s reaction or response to a particular situation or circumstance at workplace. It is the way employees conduct themselves at work.

Employees need to behave sensibly at workplace not only to gain appreciation and respect from others but also to maintain a healthy work culture. One needs to adhere to the rules and regulations of workplace.

Using the question as an example, in order to reduce the amount of non-recyclable from each office and work stations, the containers for non-recyclable wastes were removed from the offices and workstations. This has altered the employees behavior which would in turn make it difficult for the employees to practice wasteful behaviour because the situational factors has been altered.

Therefore, the option that best suits the question is option C. ALTERING SITUATIONAL FACTORS AND MAKING IT DIFFICULT TO PRACTICE WASTEFUL BEHAVIOR.

Answer:

The correct answers are the options 3 and 4:

To reprimand participants who dominate other participants

To reiterate the purpose of the discussion if it becomes vague

Explanation:

To begin with, the case that a discussion must take place in group meeting then it will depend on the subject that it will be discussed but the most probable is that a leader must be needed in order to initiate the discussion in the cases where he would need to reprimand participants who dominate other participants and also when the purpose of the discussion becomes vague. Those two are the main cases in where a leader will need to initiate and to intervene in a group meeting discussion

Answer:

The Correct Option is "B"

Explanation:

Total consumption model was created accordingly of traditional model. It shows the connection between the GDP and arranged spending. The condition of consumption model is as per the following:

Y = C + I + G + NX

Where, Y is the genuine GDP, C is Consumption, I Refers to net investment, G is government buys and NX is net ex[port.

The total use model accept that gross investment (I), government buys (G), and net export (NX) are independent to of genuine GDP (Y) as they don't depend on salary of the economy.

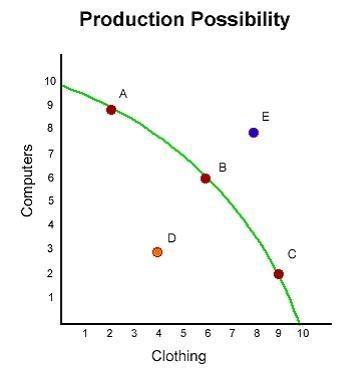

In the graph above, the point E represents values which are unattainable with current resource use and current technology.

<h3>What point is the unattainable point in the PPC?</h3>

PPC refers to production possibility curve, This is a curve that shows the relationship between available resources to what can be attained.

The points outside the curve implies that the producer cannot achieve what they want given the available resources in the economy, however if the points are within the curve the available resources can meet with the intended production

Point E is a is a point that is beyond the graph, that is outside the graph. The resources available cannot attain production.

Read more on the PPC here; brainly.com/question/21639807

#SPJ1

<h3>Complete question</h3>

This is an attachment

B., because the unemployment rate is the people who were employed