The stock of ideas in period 10 is 122.

<u>Explanation:</u>

- A stock thought is the underlying driving force to examine a potential value venture. A stock thought is the initial phase in a procedure of screening, research, and judgment that eventually prompts a choice to put or not put resources into a given stock.

-

The Stock of ideas in period t is equivalent to and is the efficiency parameter of the examination division (0.01), is the part of the populace that works in look into () and is the all out populace in the economy.

Stock of ideas = initial stock idea(1 + productivity parameter 2)^10

= 100(1 + 0.01 x 2)^10

Stock of ideas = 122.

Answer:

9.73%

Explanation:

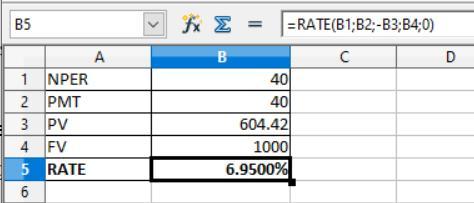

For computing the after tax cost of debt first we have to determine the cost of debt by applying the RATE formula i.e. to be shown in the attachment below:

Given that,

Present value = $604.42

Future value or Face value = $1,000

PMT = 1,000 × 8% ÷ 2 = $40

NPER = 20 years × 2 = 40 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this,

1. The pretax cost of debt is 6.95% × 2 = 13.9%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 13.9% × ( 1 - 0.30)

= 9.73%

In the Decision of Authority <span>decision-making method, group members voice their feelings and opinions, but the final decision is made by the boss or leader..

In this method, the voice of the group members only serves to give different perspectives for the leaders so they could make a decision that they believe will be better for the group</span>

Answer:

Concurrent validation

Explantion:

Concurrent validation is employed to establish documented proof that a facility and process will function as they are intended, on the basis of information gotten during actual use of the process.

Concurrent validity is a type of proof that can be assembled to justify the use of a test for predicting other outcomes.

Answer:

Profit margin

Explanation:

Profit margin = Net profits / Net sales

Company can earn insight into a company's earnings by looking at its sales strategy, pricing structure, and productivity improvements using net profit margin.