The major reason for making this type of ownership change is liability protection. A sole proprietor is personally responsible for all the debts his company generates, he can lose everything he has if he generate a big debt. In corporations, there is corporate liability shield which protects the owners of the company from loosing their personal assets as a result of business liability.

Answer:

The answer is: Knottworth Gedding should report $1,725,000 as interest expense in its 12/31/2021 income statement

Explanation:

The formula for calculating the amount of interest expense is:

interest expense = discount rate x (present value - yearly payment) x time

- Discount rate = 10%

- Present value = $40,500,000

- Yearly payment = $6,000,000

- Time = 6 months / 12 months = 0.5

interest expense = 10% x ($40,500,000 - $6,000,000) x 0.5 = $1,725,000

Answer: The Answer is D.) your opportunity cost is the time and experience of bowling

Explanation: Why it is NOT B or C is because,

Rationale: Second best. Opportunity cost is the experience you might have had if you had chosen your next-best option. In this example, the opportunity cost is the experience of the activity you did not choose – bowling.

Answer:

Difference = $9773.02

Explanation:

An annuity is a series of cash flows or payments that are of constant amount, occur after equal intervals of time and are for a limited and defined period of time. Thus, the winnings from lottery are an annuity as they pay a fixed amount $11300 every year for 21 years.

The annuity can be of two types namely ordinary annuity and annuity due. In ordinary annuity the cash flows occur at the end of the period and in annuity due, the cash flows occur at the beginning of the period. When we calculate the present value of these cash flows, it is understood that the present value of annuity due is greater than the present value of ordinary annuity.

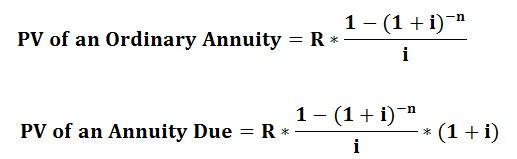

The formulas for the present value of both ordinary annuity and annuity due are attached.

In the formula, R is the annuity payment or cash flow and i is the relevant interest rate and n is the number of years or periods.

PV of annuity ordinary = 11300 * [ (1 - (1+0.1)^-21) / 0.1 ]

PV of ordinary annuity = $97730.24548 rounded off to $97730.25

PV of annuity due = 11300 * [ (1 - (1+0.1)^-21) / 0.1 ] * (1+0.1)

PV of annuity due = $107503.27

Difference = 107503.27 - 97730.25

Difference = $9773.02