Answer and explanation:

<em>Check the attached file for a well formatted answer</em>

<em></em>

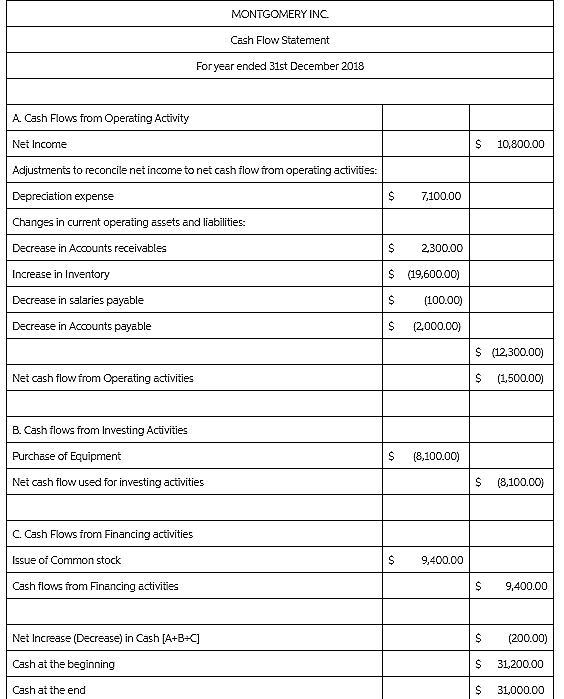

MONTGOMERY INC.

Cash Flow Statement

For year ended 31st December 2018

A. Cash Flows from Operating Activity

Net Income $ 10,800.00

Adjustments to reconcile net income to net cash flow from operating activities:

Depreciation expense $ 7,100.00

Changes in current operating assets and liabilities:

Decrease in Accounts receivables $ 2,300.00

Increase in Inventory $ (19,600.00)

Decrease in salaries payable $ (100.00)

Decrease in Accounts payable $ (2,000.00)

$ (12,300.00)

Net cash flow from Operating activities $ (1,500.00)

B. Cash flows from Investing Activities

Purchase of Equipment $ (8,100.00)

Net cash flow used for investing activities $ (8,100.00)

C. Cash Flows from Financing activities

Issue of Common stock $ 9,400.00

Cash flows from Financing activities $ 9,400.00

Net Increase (Decrease) in Cash [A+B+C] $ (200.00)

Cash at the beginning $ 31,200.00

Cash at the end $ 31,000.00

.General notes for cash flow

Cash is increased when Current liability increase or Current asset Decrease.

Cash is Decreased when Current liability Decrease or Current asset Increase.

Depreciation or loss on sale of any asset is a non cash expense hence it will be added to net income to get operating cash

Profit on sale of asset or investment is a non cash profit and hence will be deducted from operating income.