Answer: Determines the standard of life of a nation over the long term.

Explanation:

Economists believe that the economic growth of a country determines the standard of living of its people over the long term which is why measures such as GDP per capita exist.

They argue that if the economy is growing, more wealth will be created for citizens to access and the higher production of goods and services will give citizens more choice on what to buy to be able to improve their standard of living.

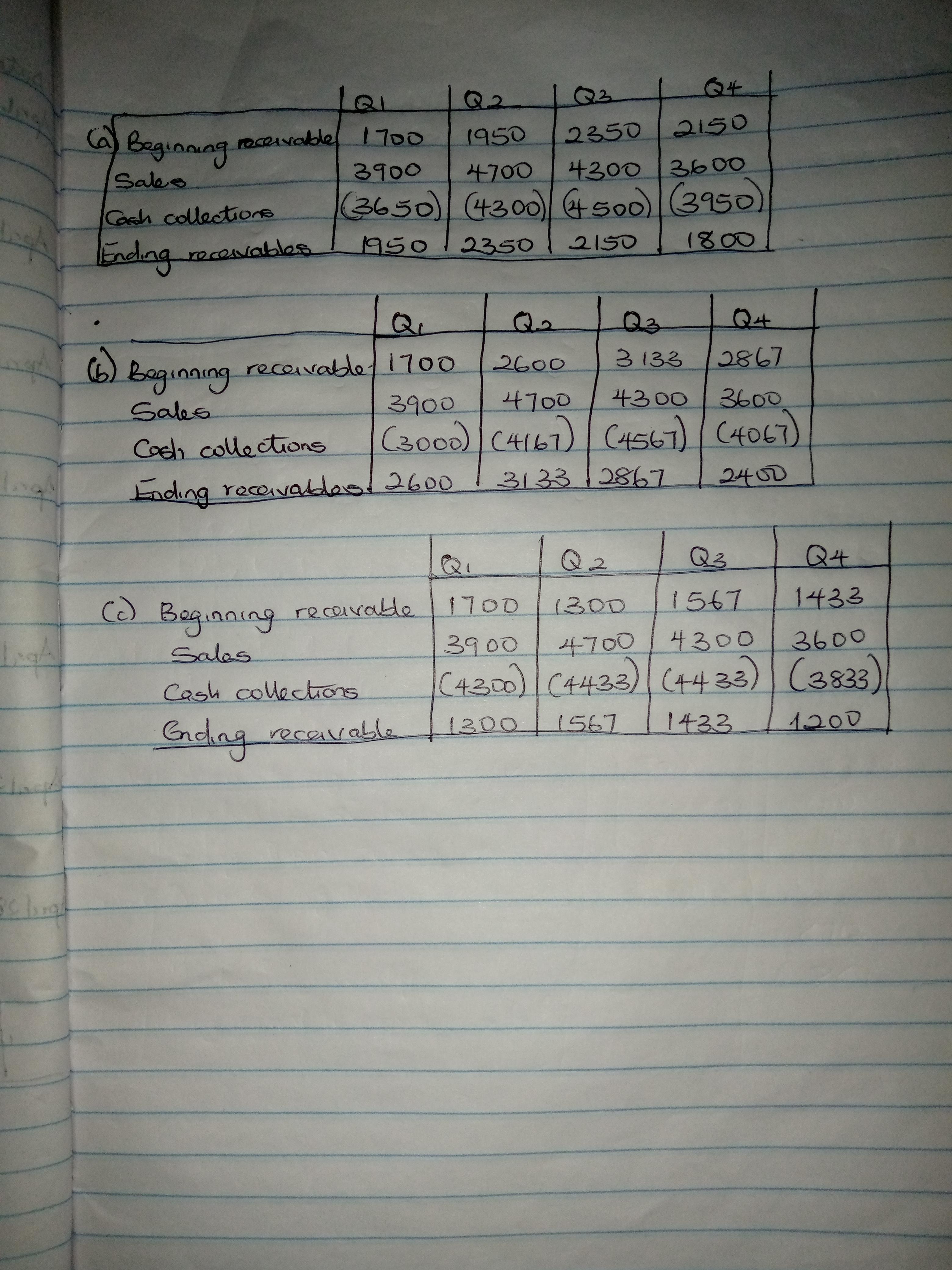

Answer: Check attachment

Explanation:

The cash collection was calculated as:

a. (90-45)/90 = 1/2

Q1 = 1700 + (1/2 × 3900)

= 1700 + 1950

= 3650

Q2 = 1950 + (1/2 × 4700)

= 1950 + 2350

= 4300

Q3 = 2350 + (1/2 × 4300)

= 2350 + 2150

= 4500

Q4 = 2150 + (1/2 × 3600)

= 2150 + 1800

= 3950

Check the attachments for further information.

Answer:

Explanation:

1. The journal entries are shown below:

Bad debt expense A/c Dr $3,378

To Allowance for doubtful debts A/c $3,378

(Being bad debt expense is recorded)

Allowance for doubtful debts A/c Dr $4,510

To Account receivable A/c $4,510

(Being written off amount is recorded)

2. The computation of the net sales is shown below:

= Gross sales - sales discount - sales return - credit card fees

= $140,756 - $1,344 - $996 - $2,129

= $136.287

Found jobs in defense industries during World War II?

Answer:

$1066.77

Explanation:

The amount that would need to be saved today is referred to as present value.

Present value is the sum of discounted cash flows

Present value can be calculated using a financial calculator

Cash flow in year 1 and 2 = 0

Cash flow in year 3 = $600

Cash flow in year 4 = 0

Cash flow in year 5 = $700

I = 5

present value = $1066.77

To find the PV using a financial calculator:

1. Input the cash flow values by pressing the CF button. After inputting the value, press enter and the arrow facing a downward direction.

2. after inputting all the cash flows, press the NPV button, input the value for I, press enter and the arrow facing a downward direction.

3. Press compute