Answer:

It increases the opportunity cost because you are foregoing more money for college.

Explanation:

Opportunity cost is the benefit profit, or value of something that is missed or given up when an individual chooses one alternative over another.

The 10% rise in salary offered by the branch manager increases the opportunity cost of going to college. This is because the higher cost (money) you could have earned by not going to college is foregone.

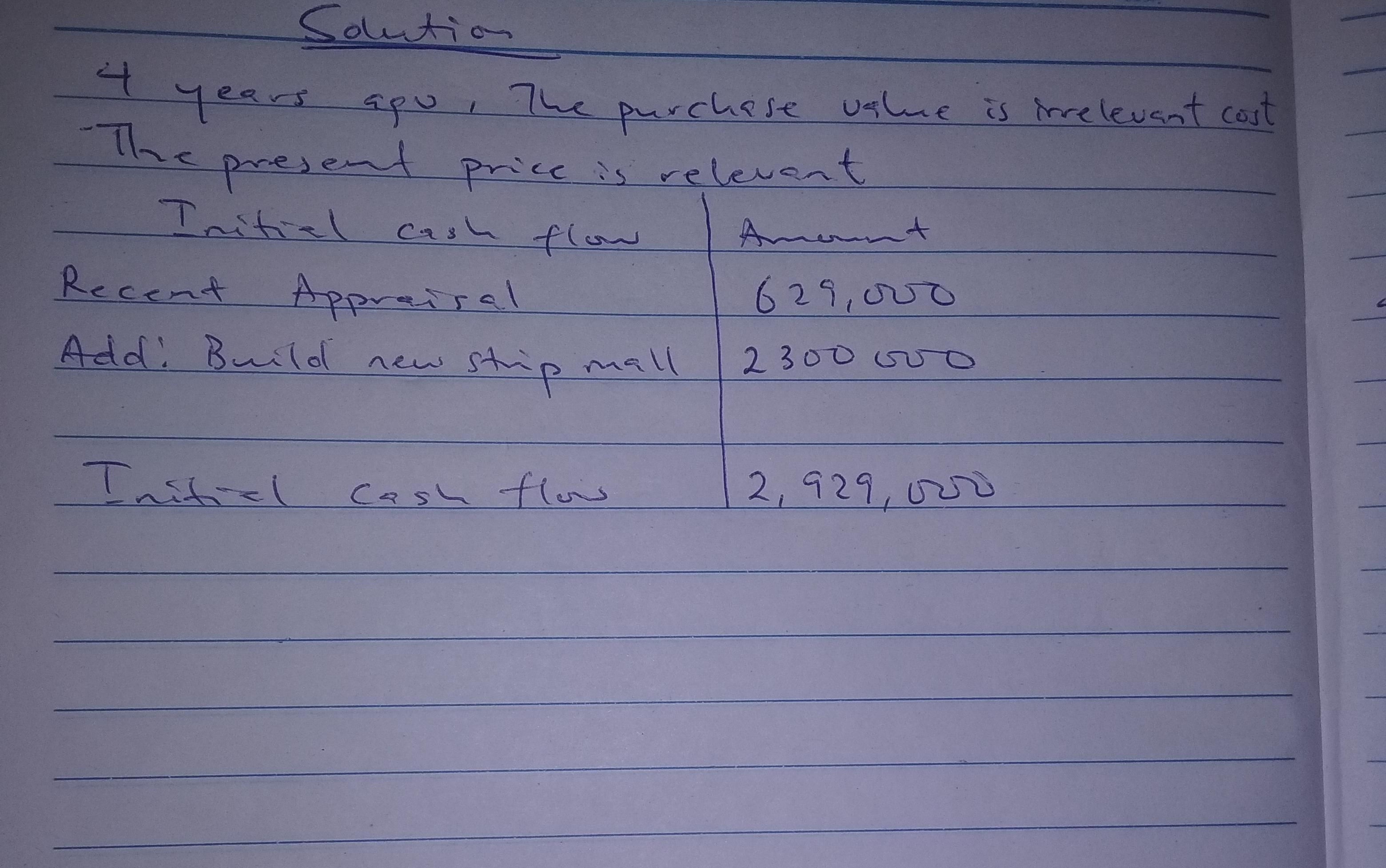

Answer:

initial cash flow is 2,929,000

Explanation:

Attached is the table

Answer:

Any type of government policy that restricts free trade and the movement of capital can trigger the aforementioned consequences. Thus, the limitation of companies to obtain economic benefits can make them decide to close their activities, leaving employees on the street (increasing unemployment), reducing the country's economic production (causing the country's real GDP to decrease), and ultimately, generating monetary lags due to lack of economic production, generating devaluations that lower the international price level of the country's products.

Answer:

Land 594,500

Explanation:

We must include all cost necessary to acquire the land and lelave it ready to use.

But, the demolition cost are associate with the old warehouse thus, as thsis asset is being destroyed It will be considered period cost, It will not be capitalized through land.

Acquisition cost 550,000

broker commission 35,000

title insurance 2,500

closing cost <u> 7,000 </u>

Total cost 594,500