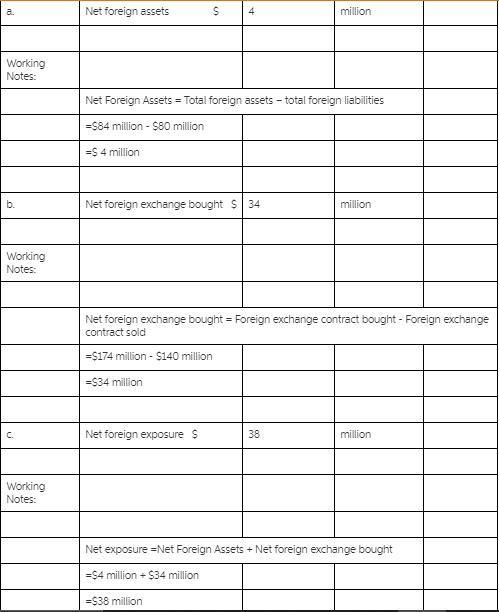

Answer:

Solution is attached below. Thanks.

Explanation:

Answer: Supply chain visibility

Explanation:

Supply chain visibility is the method used by production companies to track the exact location of a product from when it has been produced up to when the product has been successfully delivered to the buyer. With the help of supply chain visibility, the buyer can be able to track the exact location of products they ordered for, at any point in time.

Answer:

Net income= 561,506.25

Explanation:

Giving the following information:

sales of $1.67 million, cost of goods sold of $810,800, depreciation expenses of $175,000, and interest expenses of $89,575.

Tax= 35 percent

We need to determine the net income.

Sales= 1,670,000

COGS= (810,800)

Gross profit= 859,200

Depresiation= (175,000)

Interest= (89,575)

EBT= 594,625

Tax= (594,625*0.35)= (208,118.75)

Depreciation= 175,000

Net income= 561,506.25

Answer:

Date Units Unit Cost Unit Selling Price

July 1 Beginning Inventory 50 $ 10

July 13 Purchase 250 13

July 25 Sold (100 ) $ 15

July 31 Ending Inventory 200

Cost of Goods Available for sale= 250 units at $ 13+ 50 units at $ 10

= 3250 + 500= $3750

FIFO Ending Inventory $ 2600

200 units at $ 13= $ 2600

Sales 100At $ 15= $1500

FIFO Cost Of Goods Sold $ 1150

50 units at $ 10= $ 500

50 units at $ 13= $ 650

LIFO Ending Inventory $ 2450

50 units at $ 10= $ 500

150 units at $ 13= $ 1950

Sales 100 at $ 15= $1500

LIFO Cost Of Goods Sold $ 1150= Cost of Goods Available for Sale Less LIFO Ending Inventory = 3750- 2450= $ 1300

100 units at $ 13= $ 1300

Weighted Average Ending Inventory 12.5 * 200= $ 2500

Total Cost/ total units= 3750/300= 12.5

Weighted Average Cost Of Goods Sold $ 1150= Cost of Goods Available for Sale Less Weighted Average Ending Inventory = 3750- 2500= $ 1250

Weighted Gross Profit= Sales Less Weighted Cost Of Goods Sold= $ 1500- $ 1250= $ 250

<span>The company is using market-penetration pricing.</span>