Answer:

3. Foreign Direct Investment

Explanation:

Based on the information provided within the question in regards to the situation at hand, it seems that the theme park company is using a global marketing strategy called Foreign Direct Investment. This term refers to when a foreign company decides to invest in a controlling ownership of a business in another country. Just like what is going on with the theme park company wanting to buy land in Frollik in order to build an entertainment park.

If you have any more questions feel free to ask away at Brainly.

Answer:

option B

Explanation:

Prime costs refers to the expenses of a company directly linked to the labor and materials used during manufacturing. This relates to the expense of a product made, which is measured to provide a business with the highest profit margin.

A prime cost is really the cumulative direct costs of producing a commodity for sale, which can be constant or adjustable. Companies utilize prime costs as more of a method of measuring the overall cost of the development materials required to create a specific output.

Thus, from the above we can conclude that the correct option is B .

The correct option is D.

Some natural resources have been predicted that they will soon be depleted. This forecasting has not materialized because the government has increased its efforts to conserve the presently available resources and to also look for other alternatives or more of these resources.

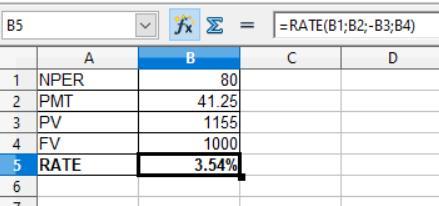

Answer:

4.96%

Explanation:

In order to determine the component after-tax cost of debt first we need to compute the before tax cost of debt by applying the RATE formula which is to be shown in the attachment below:

Given that,

Present value = $1,155

Future value or Face value = $1,000

PMT = 1,000 × 8.25% ÷ 2 = $41.25

NPER = 40 years × 2 = 80 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the above formula

1. The pretax cost of debt is 3.54% × 2 = 7.08%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 7.08% × ( 1 - 0.30)

= 4.96%

Although it is the most liquid asset, money is a flawed store of value. M1 is recognized as the measure of the money supply that is the most precisely specified.

What is term money?

Money is a good that is widely acknowledged as a means of economic exchange.

Because of inflation, money is actually an imperfect store of value. A monetary system where gold or silver, for example, is used as the actual medium of exchange. A form of money where paper money is backed by gold.

As a result, option (b) is correct.

Learn more about on money, here:

brainly.com/question/14253896

#SPJ1