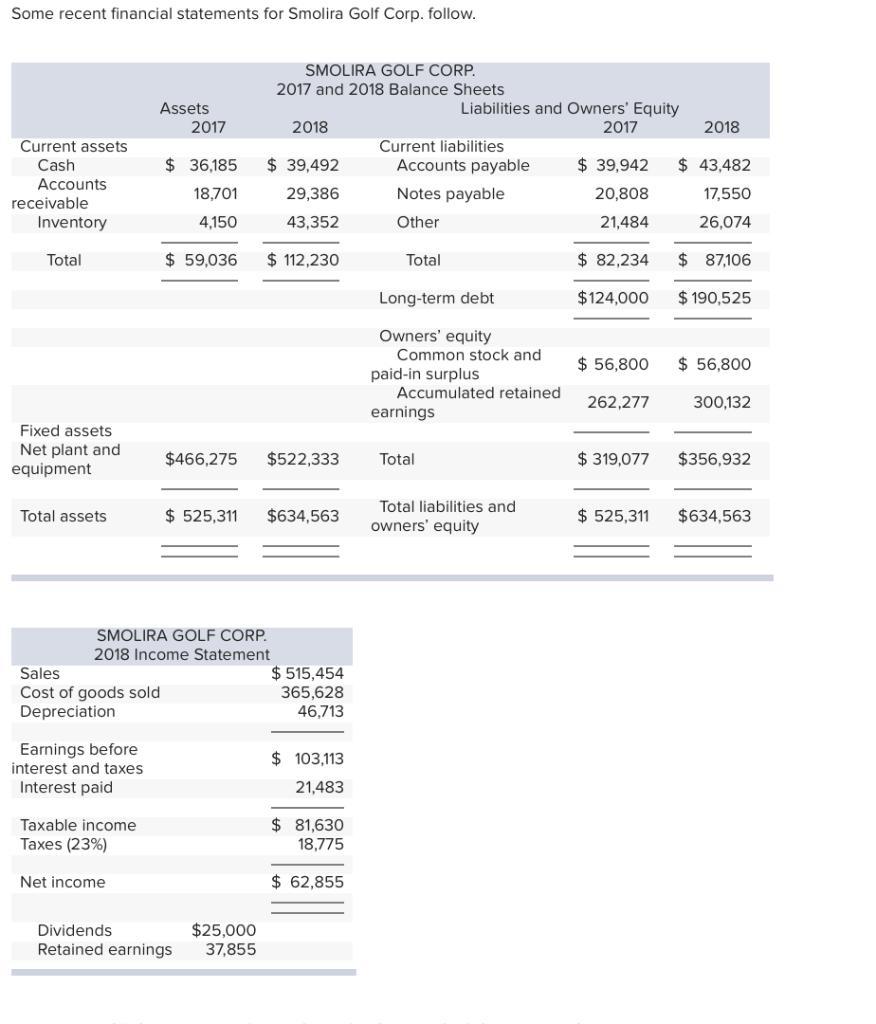

Answer:

Note: Find attach the other missing table of question

Particulars Amount$

<u>Cash flow from operating activities</u>

Income 62,855

Depreciation 46,713

Increase in AR (10,685)

Increase in inventory (39,202)

Increase in AP 3,540

Decrease in notes payable (3,258)

Increase in other CL <u>4,590</u>

Cash flow from operating activities A $64,553

<u>Cash flow from Investing activities</u>

Sale of invt

Purchase of PPE = ($102,771)

($522,333 + $46,713 - $466275)

Cash flow from Investing activities B ($102,771)

<u>Cash flow from Financing activities</u>

Issue of long term debt 66,525

Dividends Paid (25,000)

Cash flow from Financing activities C $41,525

Net change in cash & cash equivalents A+B+C $3,307.00

Opening cash and cash equivalents $36,185

Closing cash and cash equivalents $39,492