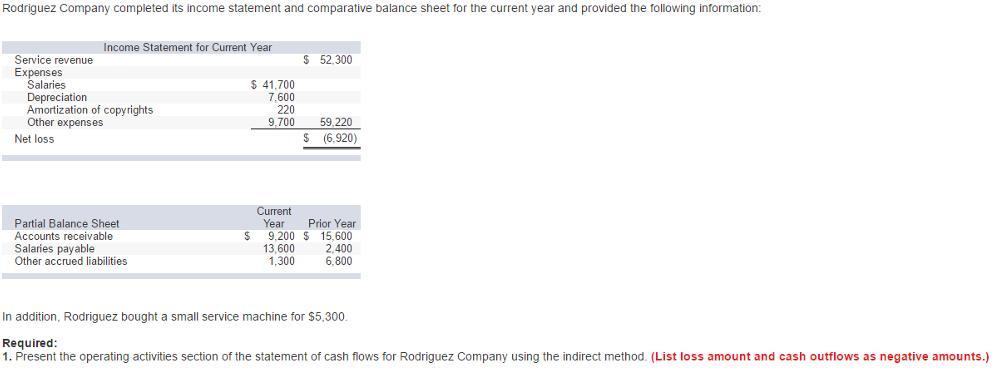

Answer:

Net Cash provided by Operating Activities = $13,000

Explanation:

Rodriguez Company

Statement of Cash flow(Partial)

Cash flows from operating activities Amount

Net Loss $(6,920)

Add: Depreciation $7,600

Add: Increase in Salaries Payable $11,200

Add: Decrease in Accounts receivable $6,400

Add: Amortization of Copy Rights $220

Less: Decrease in Other accrued $(5,500)

liabilities

Net Cash provided by Operating $13,000

Activities

Workings

Accounts receivable decrease = $15,600 − $9,200

Accounts receivable decrease= $6,400

Salaries payable increase = $13,600 − $2,400

Salaries payable increase= $11,200

Other accrued liabilities decrease = $1,300 − $6,800

Other accrued liabilities decrease = - $5,500