Answer:

The correct answers are letters "A", "B", and "C".

Explanation:

Options brokers cannot provide any strategies to investors unless the <em>Options Disclosure Document </em>(ODD) was not sent to the investor, the <em>Registered Options Principal</em> has not approved the opening of the account of the investor or if the investor intends to apply a strategy that the broker is not sure if the investor can accept the <em>risk inherent</em>.

The Options Agreement must be signed by the investor and returned to the broker within 15 days but suggestions can be provided before or after the submission of the signed document.

Answer:

$125

Explanation:

Computation for the change in net working capital

Using this formula

Change in net working capital =( Ending Current asset- Ending Current liabilities) - (Beginning Current asset- Beginning Current liabilities)

Let plug in the formula

Change in net working capital =

($493 – $272) – ($328 – $232)

Change in net working capital = $221-$96

Change in net working capital =$125

Therefore the Change in net working capital will be $125

Total assets = Current assets + Fixed Assets

Total assets = 6000+25100

Total assets = 31,100

Total liabilities = Current liabilities + Long term debt

Total liabilities = 4950+12000

Total liabilities = 16,950

According to accounting equation, stockholder's equity = Total assets - total liabilities

Stockholder's equity = 31,100-16,950 = 14,150

Value of Stockholder's equity = $14,150

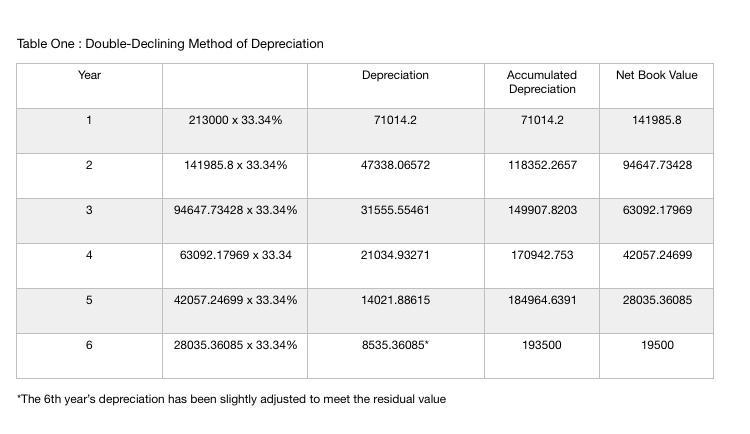

Answer:

Please refer explanation and tables attached

Explanation:

1. Double-declining balance Method:

This is where the asset's value is depreciated at twice the rate than the straight line method. The depreciation amounts would be higher in the early years of the asset's life and gradually reduce towards the end. Hence, it does not mean that the depreciation amount would be higher than the straight line basis.

Straight Line depreciation per year = 1/6* x 100 = 16.67%

*as it is useful for six years

Hence double-depreciation value = 16.67% x 2 = 33.34%

It is calculated as depreciation rate x book value of asset at the beginning of the period.

Please refer attached table one for all years depreciation.

2. Activity based depreciation is whereby an asset is depreciated based on the asset’s activity such as the number of hours worked or the number of units produced, during a particular period of time. Activity based depreciation per year is calculated as:

[(Cost - Salvage value) x activity performed during the period] / Total estimated life activity of the asset

Please refer attached table two for all years depreciation.