Answer and Explanation:

The computation of the total budgeted selling and administrative expenses is shown below;

Utilities expense $2,800

Administrative salaries $100,000

Sales commissions 5 % of sales i.e. 5% of $860,000 $43,000

Advertising $20,000

Depreciation on store equipment $50,000

Rent on administration building $60,000

Miscellaneous administrative expenses $10,000

total budgeted selling and administrative expenses $285,800

Answer:

$2,238.16

Explanation:

In the disposal of assets, gain or loss will be a comparison between the book value and the selling price.

Book value is the asset costs minus accumulated depreciation.

in this case, the book value will be

= Asset cost - Depreciation

= $31,588- $28,429.20

=$3,158.8 is the book value.

Gain or loss = selling price- book value

=$5,369.96 - $3,158.8

=$2,238.16

A gain of$2,238.16 will be gain from that sale.

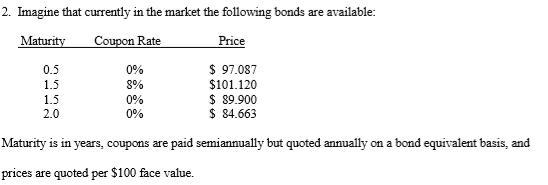

Answer:

$441,495

Explanation:

Since the information is incomplete, I looked for the missing part and found the attached information.

the current yield of a 1.5 years zero coupon bond = (100 / 89.9)¹/¹°⁵ - 1 = 0.0736 = 7.36%

the current yield of a 6 months zero coupon bond = (100 / 97.087)¹/⁰°⁵ - 1 = 0.0609 = 6.09%

now to calculate the future interest rate:

(1.0736²/1.0609) - 1 = 0.0865 = 8.65%

since we are told to determine the price of the bond:

(100/P)¹/¹°⁵ - 1 = 0.0865

(100/P)¹/¹°⁵ = 1.0865

100/P = 1.0865¹°⁵

100/P = 1.1325

100/1.1325 = P

P = 88.299

the expected price of the bond = 88.299% x $500,000 = $441,495

Answer:

The given statement is "True".

Explanation:

- The budgeting process for something like a commercial enterprise has always been based on the most recent financial statement of an organization, investment money as well as distribution channels, business objectives as well as the viewpoint in which the industry operates.

- So that the spending plan is generally more accurate unless all agencies and therefore all top executives are actively engaged.

Answer:

$12,000

Explanation:

The main difference between cash basis accounting and accrual accounting is that accrual accounting recognizes revenue only after the earning process is completed. On the other hand, cash basis accounting recognizes revenue and expenses when the money is received or paid, regardless of when the service is provided. This is why the US GAAP doesn't allow cash basis accounting.

The IRS allows cash basis accounting for individuals and small businesses that only deal with cash payments, but they must meet certain criteria:

- partnerships or C corporations with less than $5 million in yearly revenue

- sole proprietorships and S corporations with less than $1 million in yearly revenues

- family owned farms

- you provide personal services and 95% of your revenue comes from it

- no publicly traded corporation is allowed