IT IS>>>>>>>> ONLINE NEWS

If the government takes this approach, consumer surplus would increase.

A monopoly is when there is only one firm operating in an industry. A natural monopoly occurs when there is a high start-up cost associated with opening a business or a firm enjoys economies of scale.

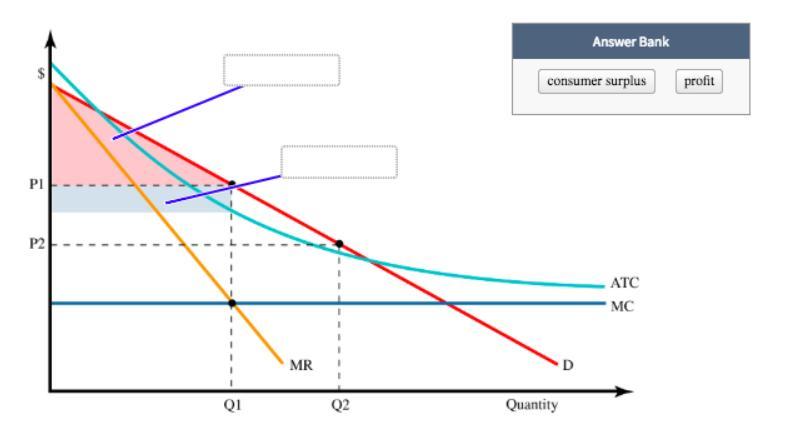

Consumer surplus is the difference between the willingness to pay of a consumer and the price of the good. As the price of a good declines, consumer surplus increases. P2 is lower than P1, this means that if price is regulated to P2, consumer surplus would increase.

Please find attached the graph required to answer this question. To learn more, please check: brainly.com/question/15415230

Answer:

The long run is best defined as a time period

- during which all inputs can be varied.

One thing that distinguishes the short run and the long run is

- the existence of at least one fixed input.

Explanation:

On the long run, all productive inputs can be changed and/or altered. that includes fixed costs like equipment and machinery, building facilities, processes, wages, etc.

On the short run, at least one of the inputs used to produce our goods or services cannot be changed, e.g. wages tend to be sticky, fixed costs (depreciation of equipment and machinery, buildings, etc.)

Answer: A company that is looking at customer trends, its competitors, and the economy to see if there are any threats or opportuntities on the horizon, and also examines its production policies and sales histories to determine its strengths and weaknesses, is conducting a <u>SWOT analysis.</u>

Explanation:

SWOT is basically the acronym for; Strengths, Weaknesses, Opportunities, and Threats. It is a very effective tool used in the business industry to form strategies. You summarized the data from internal factors to discover your strengths and weaknesses. You use the external factors to identify the threats and opportunities.

.

Tonya's company set up a booth at the college job fair to identify spring graduates who might be candidates for employment. This is an example of recruiting.

- Give candidates a chance to interact directly with the employer. Give a company the chance to evaluate the skills of a possible employee.

- All businesses must generally decide on three aspects of hiring: personnel policy, sources of hiring, and the traits and conduct of the recruiter.

- To assist your company in gaining a competitive edge through enhanced productivity, performance, and efficiency.

Employees' knowledge and abilities should be improved for their existing roles-

- Professional education

- Mentoring and coaching.

- Cross-disciplinary instruction.

- Creation of "soft skills"

Learn more about recruiting brainly.com/question/13622355

#SPJ4