Answer: Washington to exchange apples with Texas and receive money in return.

Explanation:

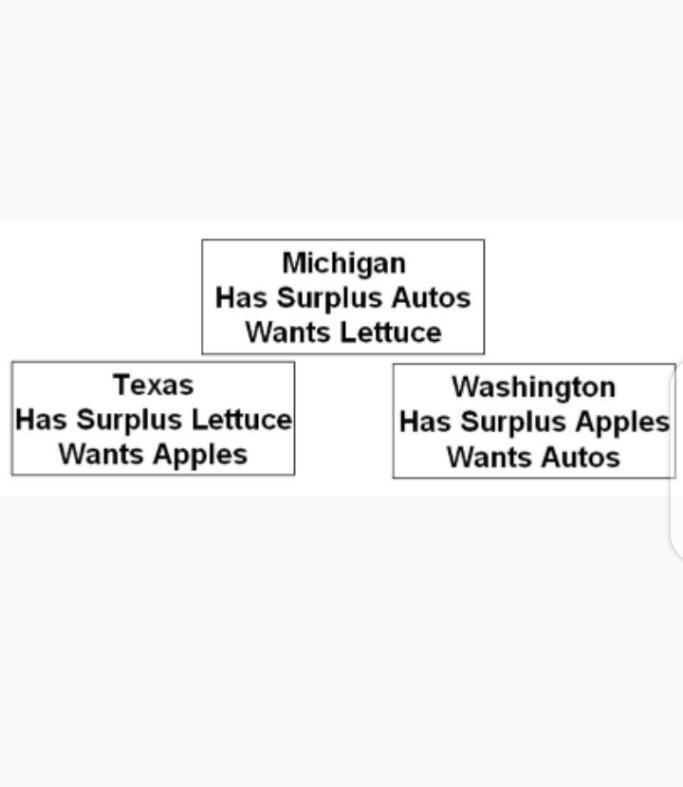

The picture relating to the question has been attached.

From the question, we are informed that Michigan has surplus autos, and wants lettuce. Texas has surplus lettuce and wants apples. Washington has surplus apples and wants autos.

If trade occurs among the three states, Washington will exchange its apples with Texas since it has surplus apples and Texas also want apples. Of the three states, it is only Washington that has surplus apples so it can exchange with Texas for money.

Answer:

4. Your house - MONEY IS THE MOST LIQUID ASSET THAT CAN EXIST

2. The funds in a savings account - MOST SAVINGS ACCOUNTS ALLOW THEIR CLIENTS A CERTAIN NUMBER OF WITHDRAWALS OR ELECTRONIC TRANSFERS PER MONTH, SO MONEY AT A SAVINGS ACCOUNT IS ALSO VERY LIQUID.

1. A bond issued by a publicly traded company - THE COMPLETE PROCESS OF SELLING A BOND MAY TAKE FROM ONE FULL DAY TO A FEW DAYS, SINCE FIRST YOUR TRADER MUST SELL THE BOND AND THEN THEY MUST TRANSFER THE MONEY TO YOUR ACCOUNT. STILL BONDS ARE LIQUID ASSETS.

4. Your house - SELLING A HOUSE IS A LONG PROCESS THAT CAN TAKE A FEW DAYS (AT BEST) TO SEVERAL MONTHS, SO A HOUSE IS NOT A VERY LIQUID ASSET.

Answer:

C) standardization strategy

Explanation:

standardization strategy can be regarded as one whereby a business owner or firm give same treatment to the whole world as if it's just one market that have just small meaningful variation It's base on an assumption that needs of people can be met with a product.