Answer: Create a sales plan that aims to enhance initial sales and market penetration with low prices based on high operational costs.

Explanation:

An emerging market is the economy of acountru that's developing and therefore,.such country is becoming more engaged with the global markets due to its growth and expansion as it grows.

The advise that'll be given to Patagonia to omit from consideration in crafting a strategy to enhance future profits in these two emerging markets is to create a sales plan that aims to enhance initial sales and market penetration with low prices based on high operational costs.

Answer

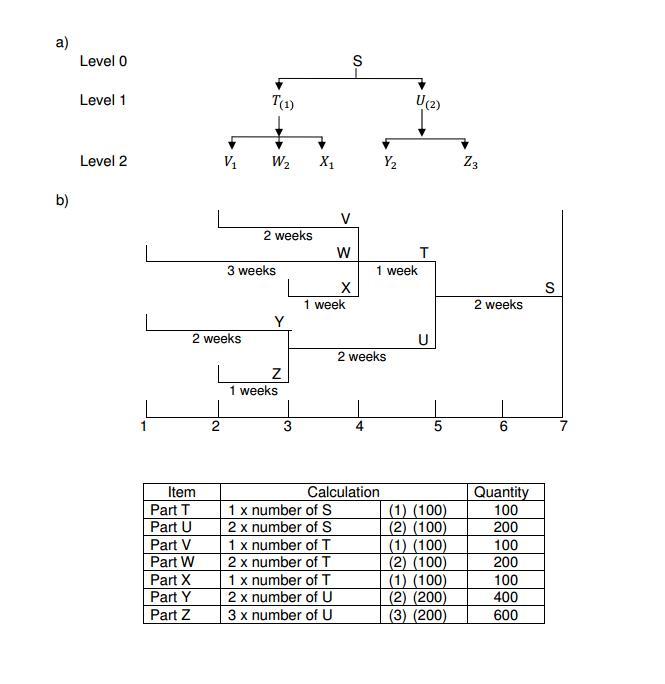

The answer and procedures of the exercise are attached in the following image.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.

The appropriate response is Allocate Resources, asset portion is an arrangement for utilizing accessible assets, for instance HR, particularly in the close term, to accomplish objectives for what's to come. It is the way toward designating rare assets among the different undertakings or specialty units.

Answer:

b. partnership

Explanation:

Partnership refers to a form of business wherein two or more individuals agree to carry out a business mutually agreeing to share profits and losses in agreed ratio as per the clauses specified in the partnership deed.

Also, upon retirement or death of a partner, the partnership firm gets dissolved and requires to be reconstituted again with necessary changes being carried out in clauses and specified profit sharing ratio in the partnership deed.

Another significant feature of partnership being, except for limited liability partnership, in all other forms of partnerships, the partners are exposed to unlimited risk.