Answer: rotate the bottom to the right, top to bottom and right to top

Explanation:

<span>given her position as the department manager, lisa has Legitimate power

Legitimate power is a type of power that derived from your formal position in your organizational hierarchy.

As a department manager, Lisa has the power to control all operational activities that heppen in her department, including arranging employees time schedule</span>

Answer:

Declining unit manufacturing costs while prices can remain high.

Explanation:

A product life cycle can be defined as the stages or phases that a particular product passes through, from the period it was introduced into the market to the period when it is eventually removed from the market.

Generally, there are four (4) stages in the product-life cycle;

1. Introduction.

2. Growth.

3. Maturity.

4. Decline.

Generally, the growth stage is the stage where the product gains acceptance from the consumer and there is a significant increase in demand and sales.

Profit margins tend to peak during the growth stage of the Product Life Cycle. This is due to declining unit manufacturing costs while prices can remain high because the product has been accepted in the market and its unit cost of production is lesser i.e they are manufactured in bulk.

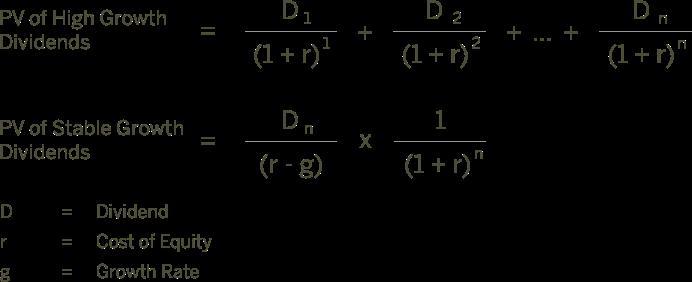

Answer:

Price of the stock today = $199.83

Explanation:

The current price of the stock can be computed using the two stage dividend growth model of the DDM approach. The DDM or dividend discount model values a stock based on the present value of the expected future dividends from the stock.

The formula for the price of the stock today using the two stage growth model is attached.

Price of the stock today = 1.95 * (1+0.2) / (1+0.12) + 1.95 * (1+0.2)^2 / (1+0.12)^2

+ 1.95 * (1+0.2)^3 / (1+0.12)^3 + ... + 1.95 * (1+0.2)^12 / (1+0.12)^12 +

[ (1.95 * (1+0.2)^12 * (1+0.09)) / (0.12 - 0.09) ] / (1+0.12)^12

Price of the stock today = $199.83

Yes I believe your scenario is correct