Answer:

Y = $391.10

Explanation:

We have 0.125<em>B</em>(n-1) = i

B(n-1) = In = 142.78

So that B(n-1) = 142.78/0.125 = 1142.24

Furthermore, B(n-1) = <em>Px = Pv </em>= P/(1+0.125) = 1142.24

P/1.125 = 1142.24

P = 1142.24*1.125

P = 1285.02.

The total amount of the loan = Principal repaid as of time (n-1) + Principal repaid in last payment

= 6009.12 + 1142.24

= 7151.36

So, the total amount of the loan is 7151.36.

The principal repaid in the first payment Y = 1285.02 - 0.125*7151.36

Y = 1285.02 - 893.92

Y = $391.10

Answer:

B. $3,750

Explanation:

Sophie will need to add up all her costs (tuition, room and board) and then add up all her funding sources (financial aid/money from parents). The difference between these two amounts is what is still owed which she will have to pay from her own savings or loans.

Costs: 11,750+11,500 = 23,250

Funding: 9000+7000+3500= 19,500

$23,250 - $19,500 = $3,750

Answer:

Explanation:

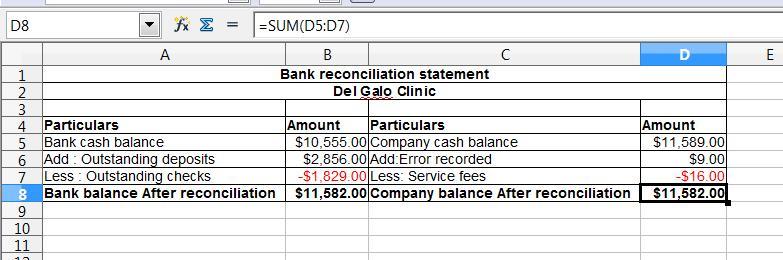

Bank Reconciliation: The bank reconciliation deals with the bank statement balance and the cash statement balance. The motive is to compare these two statements so that the organization can run in the smoothly manner.

There are various transactions due to which the bank statement balance and the cash statement balance do not match. To match these statements, we adjust the transactions accordingly.

The journal entries are shown below:

a. No journal entry required

b. Miscellaneous expense A/c Dr $16

To Cash A/c $16

(Being service charges is paid)

c. Cash A/c Dr $9 ($476 - $467)

To Utilities expense A/c $9

(Being correction is recorded)

d. No journal entry required

The preparation of the bank reconciliation statement is presented in the spreadsheet. Kindly find the attachment below:

Answer

The correct answer is C. 362

Explanation

The formular for calculating the number of shares will follow the below step

Number of Xyz share for Nick=Total dividend paid per year/the dividend on a single share

Total divident paid=$1567.46

Divived on a single share=$4.33

Total number of shares=$1567.46/$4.33=362 shares