If a government is trying to encourage economic growth, they would do all of these things except raise taxes. Raising taxes has the opposite effect and will slow growth because it takes more money out of the economy that could be used for growth and expansion.

Answer:

Hence, The division's return on investment (ROI) is closest to 32.7%

Explanation:

Return on Investment : It show a ratio between net operating income and average operating assets so that company get to know how much the return is available during a period.

The formula to compute return on investment is shown below:

= Net operating income ÷ Average operating assets

= $1,141,700 ÷ $3,495,000

= 32.7%

Since the total sales and require rate of return is irrelevant while computing the ROI. So, it would not be considered in computation part.

Hence, The division's return on investment (ROI) is closest to 32.7%

Answer and Explanation:

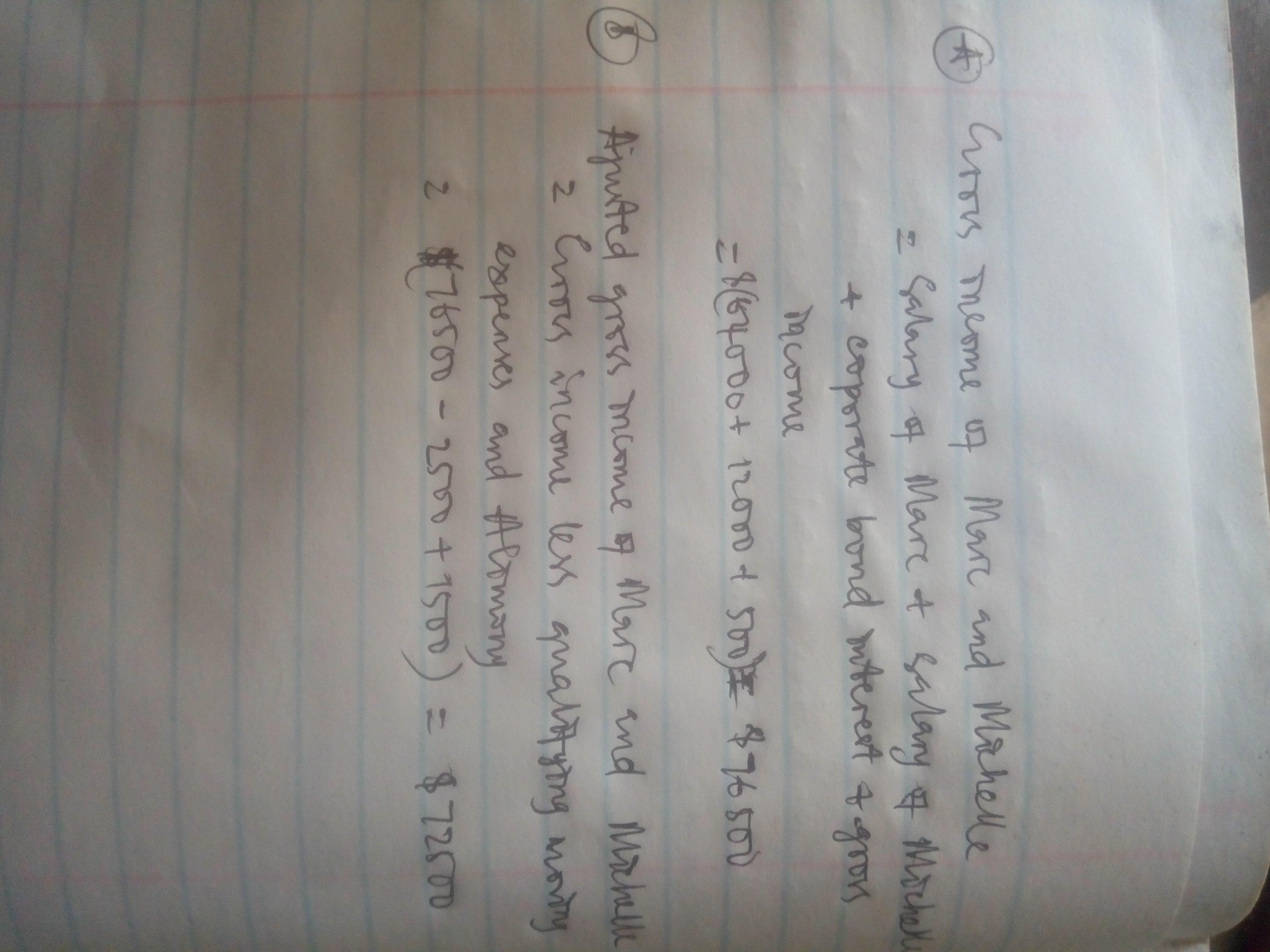

Adjusted gross income abbreviated AGI is the tax payers gross income minus deductions used in arriving at taxable income(AGI less allowable deductions)

Please find attached calculations for gross income and AGI for the couple

Answer:

boundary spanning

Explanation:

Boundary spanning -

The term boundary spanning was given by Tushman in late 1950's .

It is the term used to describe an individual in the innovation system , whoes role is to link the internal work of the organization with the external work .

From the statement of the question , the example is for the term boundary spanning .