Answer:

<u>Supply chain management</u>

Explanation:

Supply chain management refers to a system of organizations, people, activities and information which are involved in the movement of products from the suppliers to the customers.

Such activities transform the inputs into finished products which are delivered to the end customers.

Logistics refers to the activities concerned with efficient movement and transportation of goods and products to the customers. This involves making the product available when and where required and within a specified time frame to yield customer satisfaction.

Operations management is conerned with ensuring effcient business operations with optimal utilization of resources and minimum possible wastage.

Marketing channel management refers to channels of distribution to be selected for making goods and products available such as wholesellers, retailers, etc.

Thus, supply chain management integrates the functions of logistics management, operations mangement, marketing channel management and supply management, to ensure products are available in the right quantities, at right places and at the right times.

Answer: Preview-view-review strategy.

Explanation: The preview-view-review strategy is used in many different learning environments. This process allows the presenter or teacher to preview the information that will be covered, go over the information being discussed and then review it as a conclusion at the end. By previewing the information, the audience is able to understand what topics will be covered, then learn about them in the view stage and have a summary of the information covered in the review.

Answer:

sender

Explanation:

Based on the information provided it can be said that Daimler Chrysler was the sender of the message in this communication process. This can be said because Daimler was the one who launched the campaign that was used to target these consumers and garner their interest towards the product they are selling.

Full question attached

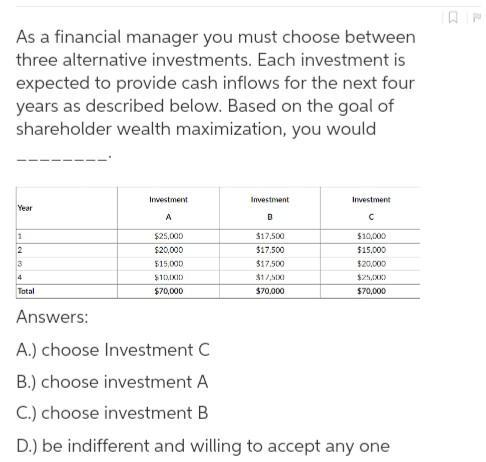

Answer:

B. Choose investment A

Explanation:

Looking at the investment cash flows for the four years, investment A maximises the shareholders wealth mostly because it covers cost of investment quicker than other investments B, C and D. It begins with the highest cash flow return, for first and second year therefore pay back period is lower with investment A. Also net present value is higher.

Answer:

Price packs

Explanation:

- a type of sales promotion where customers are given a discount off the product's regular price; the discount is typically marked, or "flagged," prominently on the label or package; also known as a "cents-off" deal.

- Price packs are sales promotions that provide consumers with a reduced price that is marked directly on the package by the manufacturer.

- Here two or more products are given together at the price of one or at discounted rates.

To learn more about it, refer

to brainly.com/question/25689052

#SPJ4