Answer: The corrects answers are "a commodity futures contract", and "a call option on Intel stock".

Explanation: An example of a derivative security is a commodity futures contract, and a call option on Intel stock.

There are several types of derivative securities. A derivative security is a financial product whose value depends on the value of another asset. They can be classified in several ways, depending on their complexity, their characteristics or the agents involved in them.

Answer:

Large most likely reports net cash outflows from investing activities of $9 million.

Explanation:

Large Corporation

Statement of cash flows (extract)

$ in millions

Purchase of patent ($14)

Proceeds from sale of land and buildings 24

Cash paid to acquire office equipment (19)

Net cash flows from investing activities ($9)

Note that the purchase of treasury stock belongs to financing activities section of the cash flows, while gain from sale of land and buildings and investment revenue belong to operating activities section of the cash flows

Answer: The answer is provided below

Explanation:

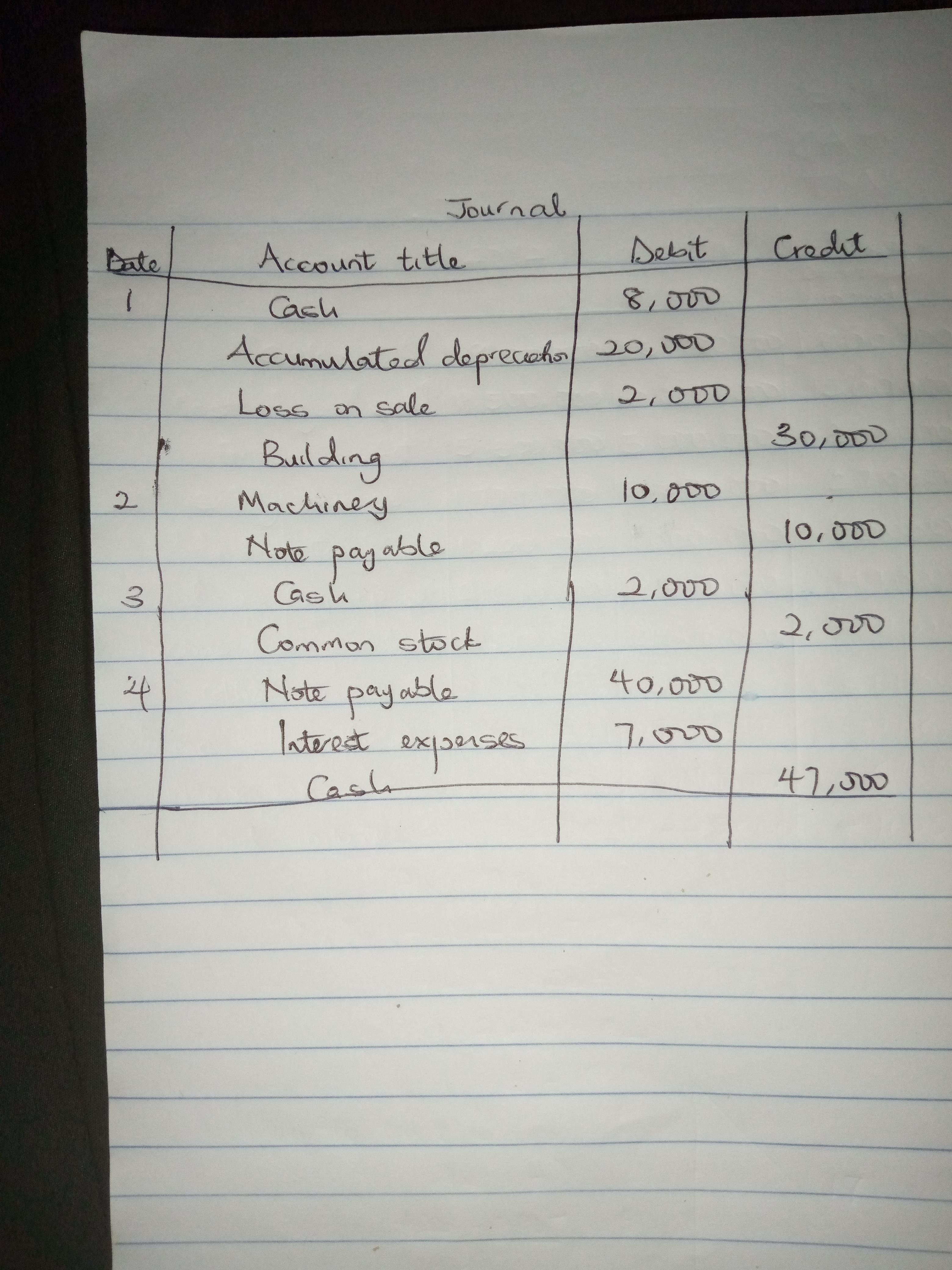

a. The reconstructed journal entry has been prepared and attached.

b. The following are the effects it has on the investing section or the financing section of the statement of cash flows.

The first transaction will lead to a cash inflow of $8,000 from the investing activities.

The second transaction is non-cash transaction therefore, it will not be reported in either the financing or the investing activities.

The third transaction will lead to a cash inflow of $2,000 from the financing activities.

The fourth transaction will lead to a cash outflow from the financing activities.

Thw diagram has been attached.

Answer:

a. Debt Equity ratio is calculated by dividing long term Debt by total equity of the company.

b.Equity Multiplier or P/E ratio=Market value per share/Earning per share.

Explanation:

a. Debt Equity ratio is calculated by dividing long term Debt by total equity of the company. The Debt Equity ratio can be calculated using the Market value of debt or equity. It can also be calculated using the book values of debt or equity which are included in the balance sheet of the company.

b. Equity multiplier is also known as price /earning ratio. A price/earnings ratio or P/E ratio is the ratio of the market value of a share to the annual earnings per share. For every company whose shares are traded on a stock market, there is a P/E ratio. For private companies (companies whose

shares are not traded on a stock market) a suitable P/E ratio can be selected and used to derive a valuation for the shares.

Equity Multiplier or P/E ratio=Market value per share/Earning per share.