Answer:

Hello some parts of your question is missing attached below is the missing part

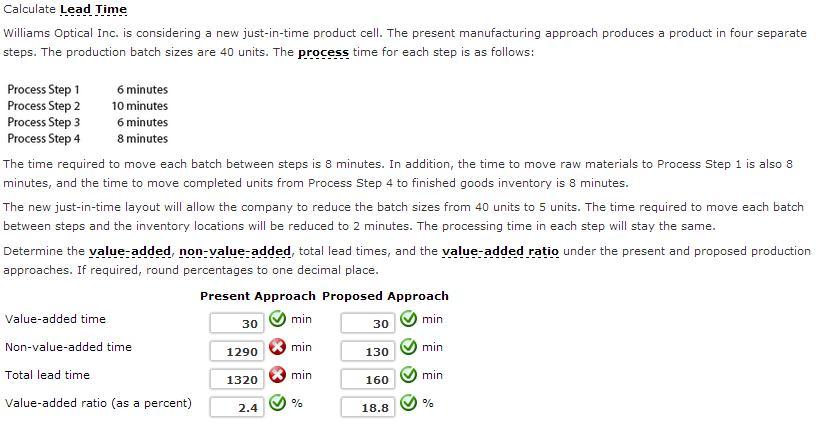

Answer : value added times : 30 minutes , 30 minutes

non-value added times: 1210 minutes, 130 minutes

Total lead times : 1240 minutes, 160 minutes

value added time as a ratio: 2.4%, 18.8%

Explanation:

Given data:

production batch sizes = 40 units

process step 1 = 6 minutes

process step 2 = 10 minutes

process step 3 = 6 minutes

process step 4 = 8 minutes

Determining : The value added, non-value added , total lead times and value added ratio under the present and proposed production approaches

UNDER PRESENT PRODUCTION APPROACH

Th value added time:

= summation of all process times = (6+10+6+8) = 30 minutes

Non-value added time:

= Value added time *(Batch size -1) + move time between each step

= 30*39+8*5

= 1170 +40 = 1210 minutes

total lead time :

= value added time + non-value added time

= 30 + 1210 = 1240 minutes

value added time as a percentage/ratio

(value added time / total lead time) * 100

= 30 / 1240 * 100 = 2.4%

UNDER PROPOSED PRODUCTION APPROACH

value added time :

= summation of all process times = (6+10+6+8) = 30 minutes

Non-value added time :

= Value added time *(Batch size -1) + time between each step

= 30*4+2*5 = 120 + 10 = 130 mins

total lead time :

= value added time + non-value added time = 30 +130 = 160 mins

value added time as a percentage/ratio:

(value added time / total lead time ) * 100

= (30 / 160) * 100 = 18.8%