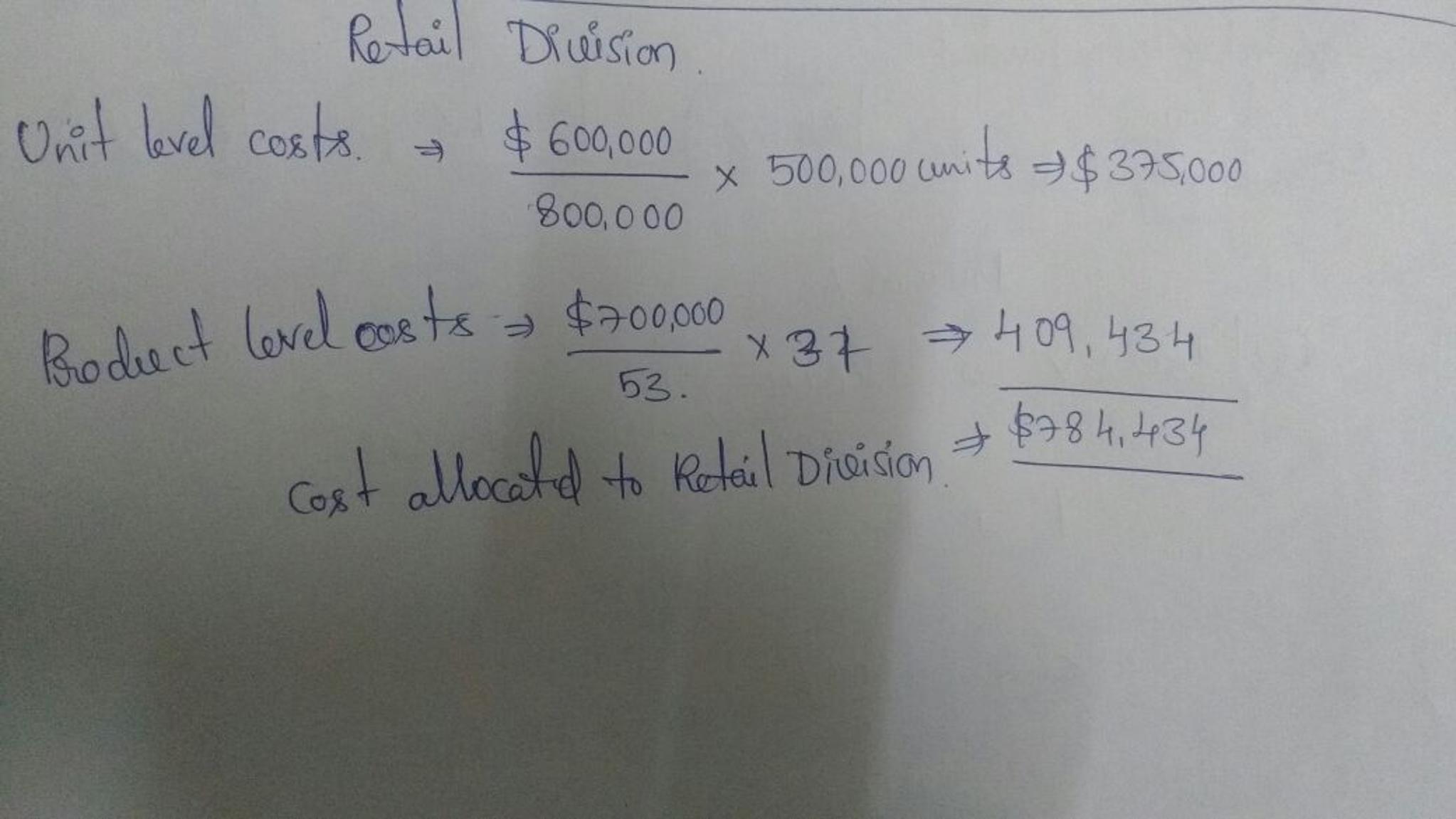

Answer:

She may use <u>$250, 000 </u>of the $278, 000 proprietorship business loss to offset non-business

Income. Liesel has an excess of<u> $28, 000</u>. The excess business loss is treated as part of her NOL [Net Operating Loss] and is to carry forward the $28, 000.

Explanation:

She may use $250, 000 of the $278, 000 proprietorship business loss to offset non-business

Income. Liesel has an excess of $28, 000. The excess business loss is treated as part of her NOL [Net Operating Loss] and is to carry forward the $28, 000.

The Tax Reform Act of 1986, sets limitations on losses when someone is the passive owner of a business entity. However, limitations are now also set for non-passive owners according to the Tax Cuts and Jobs Act of 2017.

The Tax Cuts and Jobs defines Excess Business Loss as follows:

The aggregate deductions for the year attributable to the taxpayer’s businesses

Less: The sum of aggregate gross income or gain of the taxpayer

Less: A threshold amount ($500,000 for married taxpayers filing a joint return,

$250,000 for all other taxpayers).

This threshold amounts are adjusted for inflation yearly.

The purpose of this limitation on business loss is to put a limit on non-business income. Examples of are interest, salaries, dividends and capital gains.

So, of Liesel’s $278, 000 proprietorship loss, only $250, 000 can be used to setoff the non-business income. The balance of $28, 000 is treated as part of her net operating loss. This loss will be carried forward in the subsequent years.

For years after 2017, the NOLs are limited to 80% of the pre-NOL taxable income. The Net Operating Losses are carried forward indefinitely