A.

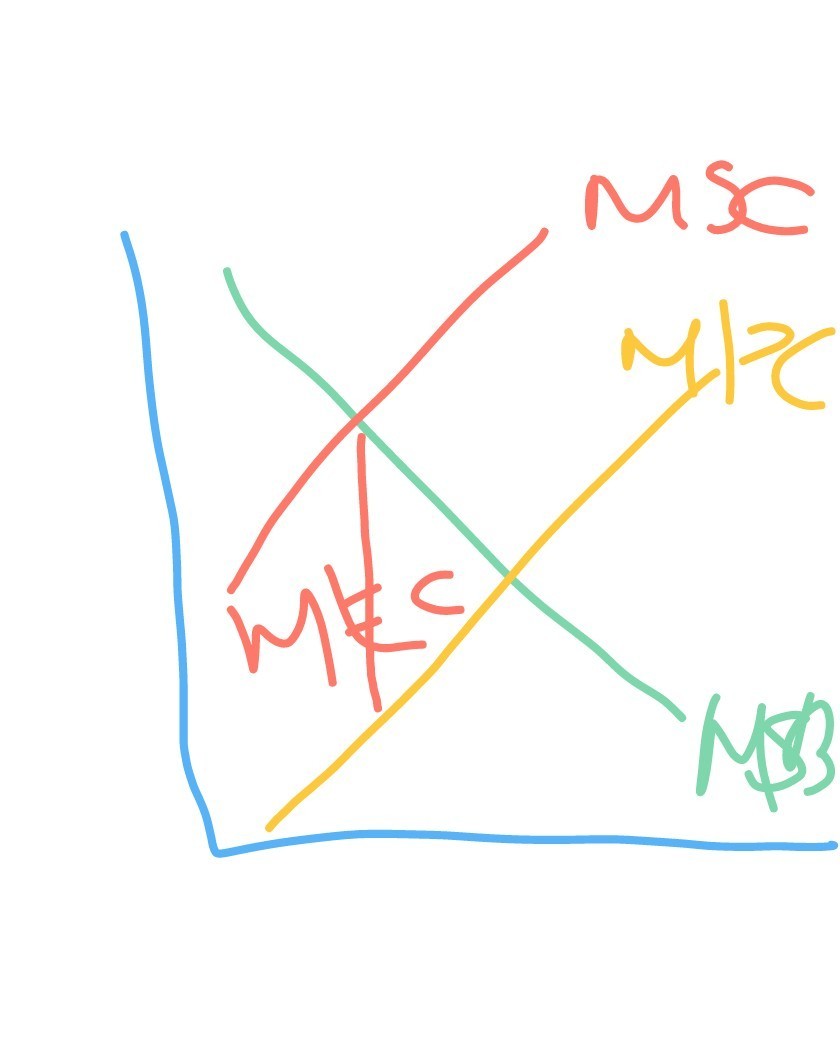

If you recall, negative externalities arise when there is a divergence between marginal private cost and marginal social cost, the difference being the marginal external cost as shown from the poorly drawn diagram. If we got rid of the marginal external cost by producing less, then the externality would dissipate.

However, the question is weird as there are no options for compensation. What would rather happen is that whoever has the property rights will be compensated the size of the MEC and there would be social welfare, whereas the question only tackles removing the externality through stopping production.

Answer:

Debit Cash $1,261

Dr card discount expense $39,

Credit Sales Revenue for $1,300

Explanation:

Stelloh's Berry Farm Journal entries

Debit Cash $1,261

($1,3,00-$39)

Dr card discount expense $39,

(3%×$1,300)

Credit Sales Revenue for $1,300

Answer:

The answer is letter B

Explanation:

Relationships involving income statement accounts tend to be more predictable than relationships involving only balance sheet accounts.

Because analytical procedures are evaluations of financial information made by study of plausible relationships among financial and nonfinancial data using models that range from simple to complex. The reason is that income statement amount is based on transactions over a period of time, but balance sheet amounts are for a moment in time. Moreover, amounts subject to management discretion tend to be less predictable.

Answer:

A. rose 60% from the cost of the market basket in the base year.

Explanation:

The base year of 1982-1984 represents a 100 value for the index, and anything above it, is an over 100 value.

A 60% rise in 12 years (1984 to 1996) represents an average inflation rate of 5% every year, a bit high, but still within a moderate range.

The formula to find the adjusted consumer price index is:

Adjusted CPI = (CPIn / CPIb) - 1

Where:

CPIn = consumer price index in selected year (in this case 1996)

CPIb = consumer price index in base year (in this case 1982-1984)

A decrease in demand and an increase in supply will cause a fall in equilibrium price, but the effect on equilibrium quantity cannot be determined. For any quantity, consumers now place a lower value on the good, and producers are willing to accept a lower price; therefore, price will fall.