Answer:

The correct answer is A

Explanation:

Change in accounting principle is the term which is defined as when the business choose among the GAAP (generally accepted accounting principles) or changes the method with which the principle is used. These principles impact the way or the method used, and then estimates the particular recalculation.

For example, company using the different method of depreciation after the 1st year of operations pr switching among FIFO to LIFO methods of inventory valuation.

So, in this case, the company switch or change the completed contract method to the percentage of completion accounting method. Therefore, the company uses the change in the accounting principle.

Answer:

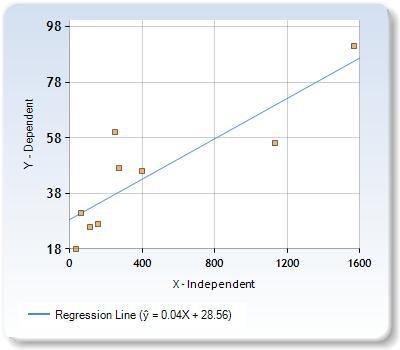

H0 : β = 0

H1 : β = 0

R = 0.8642

P value = 0.002654

Explanation:

Null hypothesis : H0 : β = 0

Alternative hypothesis : H1 : β ≠ 0

The correlation Coefficient, R value as obtained using a correlation Coefficient calculator is 0.8642. This depicts that a strong positive relationship exists between court income and Justice salary.

The Pvalue using the Pvalue calculator (R = 0.8642, N = 9) = 0.002654

The Pvalue < α

0.002654< 0.05 ; Hence, we reject H0.

Answer:

Option D is false

Explanation:

You can prevent client codes from creating objects of a class by providing a single private constructor that consists entirely of static fields and methods for example

public class Validation

{private Validation() {} // prevents instances // static methods and fields go here}

Answer:

3.8%

Explanation:

3 year bonds yielding 3.2%

6 year bonds yielding 5.0

Annual pay bond 4 years

Yielding bond+[(Annual pay bond- Bonds years)/bond years]×(Yielding bond-Yeilding bonds)

Let plug in the formula

Interpolating: 3.2% + [(4 - 3) / (6 - 3)] × (5.0% - 3.2%)

=3.2%+[1/3×(1.8%)]

= 3.2%+(0.33333×1.8%)

=3.2%+0.006

=0.032+0.006

=0.038×100

=3.8%

Alternatively,

Interpolating: 3.2% + [(4 - 3) / (6 - 3)] × (5.0% - 3.2%) =3.8%

In this case the analyst should estimate a YTM for the non-traded bond that is closest to: 3.8%

<h3><u>Answer;</u></h3>

B. both total assets and total liabilities and owner’s equity.

<h3><u>Explanation;</u> </h3>

A double-ruled line should be drawn under the amount for both total assets and total liabilities and owner’s equity.

A single ruled line should be drawn on the column line above the amount for total assets, total liabilities and total liabilities and owner' equity.

For a given date, the Balance sheet shows the; total assets, total liabilities and owner's equities. That is, the Balance sheet shows end-of-period balances in the firm's Assets, Liabilities, and Owners Equity accounts