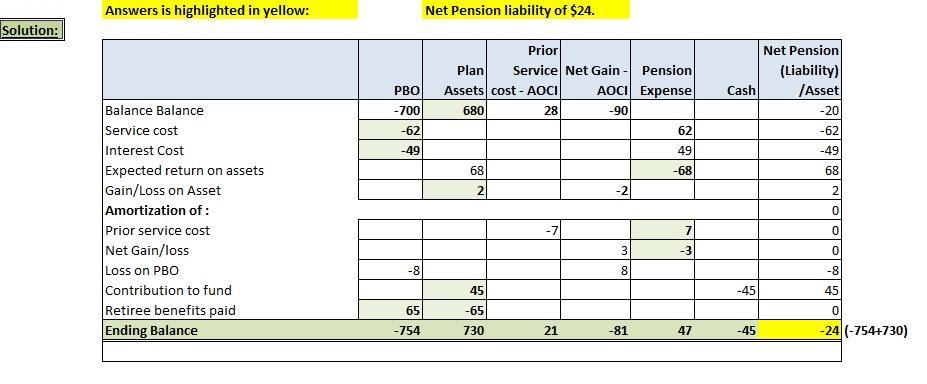

Answer:

Martinez, Inc. acquired a patent on January 1, 2017 for $41,800 cash. The patent was estimated to have a useful life of 10 years with no residual value. On December 31, 2018, before any adjustments were recorded for the year, management determined that the remaining useful life was 6 years (with that new estimate being effective as of January 1, 2018). On June 30, 2019, the patent was sold for $26,800. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.)

Required:

a. Prepare the journal entry to record the acquisition of the patent on January 1, 2017.

b. Prepare the journal entry to record the annual amortization for 2017.

c. Compute the amount of amortization that would be recorded in 2018. (Round your final answer to the nearest whole dollar.)

d. Determine the gain (loss) on sale on June 30, 2019. (Round your intermediate calculations and final answer to the nearest whole dollar.)

e. Prepare the journal entry to record the sale of the patent on June 30, 2019. (Round your intermediate calculations and final answer to the nearest whole dollar.)

a) Journal Entry to record acquisition of patent:

January 1, 2017:

Debit Patent Account with $41,800

Credit Cash Account with $41,800

Being acquisition of patent with cash

b. Prepare the journal entry to record the annual amortization for 2017.

Annual amortization = $41,800/10 years = $4,180

Journal entry to record the annual amortization for 2017:

December 31, 2017

Debit Amortization Expenses with $4,180

Credit Accumulated Patent Amortization with $4,180

Being 2017 amortization expense.

c. Compute the amount of amortization that would be recorded in 2018. (Round your final answer to the nearest whole dollar.)

New amortization for 2018 would be ($41,800 - $4,180) /6 years = $6,270

d. Determine the gain (loss) on sale on June 30, 2019. (Round your intermediate calculations and final answer to the nearest whole dollar.)

Loss on sale on June 30, 2019:

Patent Account minus accumulated amortization to date

2019 Amortization up to June 30, 2019 = $6,270/2 = $3,135

Accumulated amortization = 2017 + 2018 + 2019 amortizations

= $(4,180 + 6,270 + 3,135) = $13,585

Patent Book Value = $41,800 -$13,585 = $28,215

Loss on sale = Sales minus book value = $(26,800 - 28,215) = ($1,415)

e. Prepare the journal entry to record the sale of the patent on June 30, 2019. (Round your intermediate calculations and final answer to the nearest whole dollar.)

Journal entries to record the sale of the patent on June 30, 2019:

June 30, 2019:

Debit Cash with $26,800

Debit Loss on Sale with $1,415

Credit Patent Account with $ $28,215

Being cash and loss realized on sale of patent.

Debit Amortization with $3,135

Credit Accumulated Amortization with $3,135

Being amortization expense for 6 months.

Debit Accumulated Amortization with $13,585

Credit Patent Account with $13,585

Being entries to close the accounts.

Explanation:

Amortization is the depreciation term for intangible assets. While tangible assets are depreciated over their useful life, intangible assets are amortized.

The essence is to match revenue over the periods for which the cost was incurred in accordance with GAAP.

Similar treatments are given to amortization like depreciation, including annual expensing, accumulation, and loss and gain on sale or retirement of the intangible.