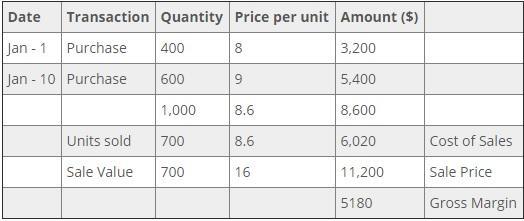

Answer:

A. USD 5,180/-

Explanation:

In the actual method of inventory valuation, the inventory reaming and the COGS (Cost Of Goods Sold) is measured after each purchase or sale of a transaction. So the COGS and the remaining value of the inventory is known all the time.

Formula:

- Gross margin is equal to Sales minus COGS

Answer:

The correct answer is option A.

Explanation:

The bureau of labor statistics works under the department of labor. It collects information regarding, unemployment rate, types of employment, etc. It provides monthly data on the unemployment rate.

The BLS considers people who are jobless, actively looking for work and available for work as unemployed. Those people who are jobless and not actively looking for work are considered discouraged workers. These workers are not included in the labor force.

The unemployment rate is calculated as the ratio of a number of unemployed workers to the total labor force.

In the survey by BLS, some discouraged workers falsely report themselves as actively looking for work even when they are not. These workers get included in unemployed workers and the total labor force. This causes the unemployment rate to be overstated.

Answer:

a. 2.63

b. 139 days

Explanation:

a. Inventory Turnover is a ratio that measures how often inventory is replaced by a company. A higher ratio is good because it means that the company is selling more.

Formula;

=

=

=

= 2.63

b. Days in Inventory refers to the amount of time that stock remains in the company before it is sold. This is preferred to be lower as opposed to higher.

=

=

= 138.78

= 139 days

Answer: Content

Explanation:

The content validity is the is one of the important methodology that is use for recognize and also evaluate the given content properly. The content validity is statistically evaluate and test the assessment through the subject matter expert.

The content validity measure the knowledge in the domain of the content. According to the question, checking the new content based on the relevant literature that providing the content validity.

Therefore, Content validity is the correct answer.

<span>A country's ability to meet its financial obligations is the main determinant of its "economic risk". Whether a country will be able to repay debts which it takes on, such as in the form of bond issues, is a key driver of the willingness of investors to make capital contributions to a country, and the return that they expect in exchange for assuming that risk.</span>