If the government takes this approach, consumer surplus would increase.

A monopoly is when there is only one firm operating in an industry. A natural monopoly occurs when there is a high start-up cost associated with opening a business or a firm enjoys economies of scale.

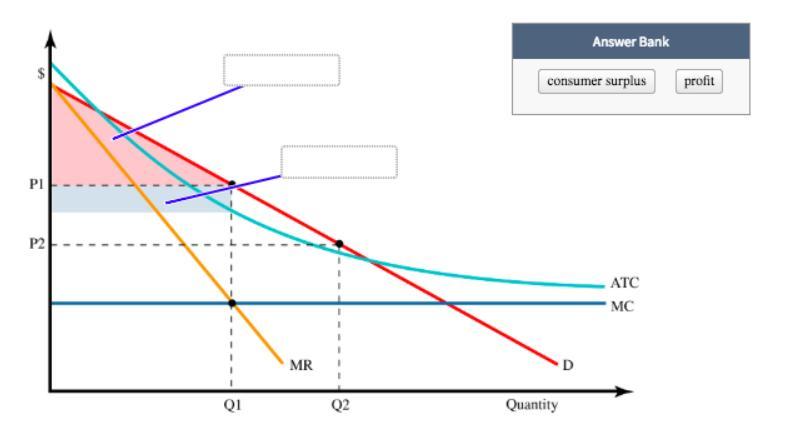

Consumer surplus is the difference between the willingness to pay of a consumer and the price of the good. As the price of a good declines, consumer surplus increases. P2 is lower than P1, this means that if price is regulated to P2, consumer surplus would increase.

Please find attached the graph required to answer this question. To learn more, please check: brainly.com/question/15415230

Answer: A customer strategy

Explanation: In simple words, it refers to a strategy under which an organisation tries to understand the needs and wants of the customers more carefully with the objective of maximizing their utility satisfaction.

Under this strategy, organisation tries to increase the financial value of their product that the customer percieves after buying it.

Hence the correct option is E.

Answer:

Budgeted Production is obtained by adding Sales to the desired finished goods inventory and subtracting beginning finished goods inventory.We move opposite to get to the budgeted production .

For example if we have $ 300,000 sales and desired ending inventory is $ 50,000 and finished good beginning inventory is $ 25,000 so the budgeted production would be

Budgeted Production = Sales + Desired Ending Inventory - Beginning Inventory

Budgeted Production = $ 300,000 + $ 50,000- $ 25,000= $ 325,000

Clicktivism optimists point out how the internet vastly expands the range of political commentary. The term clicktivism is used to denote the use of social media and other online methods to <span>use to advance social causes and </span><span>promote a cause.

</span><span> Example is when activists are using social media to organize a protest.</span>

The main difference between service companies and retail or manufacturing companies is that retailers and manufacturers must account for;

- Inventory and Cost of Goods

Inventory refers to the goods in stock which the business wishes to sell in order to make a profit from.

Retailers and manufacturers produce items that will be sold and these items need to be stocked somewhere till the need for them arises.

The same is not applicable to service companies because they do not have physical goods to sell.

Also, the cost of goods refers to the direct cost of producing goods. Since service companies do not produce goods, this is not accounted for.

Learn more here:

brainly.com/question/15015056