Answer:

a. 1,090

Explanation:

Without any other information provided, the easiest way to answer this question is to make directly the calculations of income and costs. the logic behind this problem is to calculate all the income and substract the costs of production, in this particular case we have:

+Income: 3,250

-Cost of goods: 1,285

-Operating expenses: 875

Net Income: 1,090

Answer:

the investment's coefficient of variation is 1.25.

Explanation:

The coefficient of variation relates the units of return to the units of risk. It expresses the unit of risk per 1% of return as follows :

<em>Coefficient of Variation = Standard Deviation ÷ Return</em>

Therefore,

Coefficient of Variation = 10 ÷ 8

= 1.25

The phenomenon experienced by the client when he believed that the performance appraisal was unfairly influenced by a drug error that the employee committed several weeks ago, is called the Horns Effect.

<h3>What is the Horns Effect?</h3>

The Horns Effect is a rater bias property in performance appraisal at workplace. It is a tendency for a single negative attribute to influence the rater to mark everything on the lower side of the scale. It is a bias that makes them think that one bad attribute seems to spoil the bunch.

It is the exact opposite of Halo Effect and makes decision making challenging. Horns Effect may lead to unfair sanctions or inappropriate dismissal of the employee.

To know more about Horns Effect, visit:

brainly.com/question/988504

#SPJ4

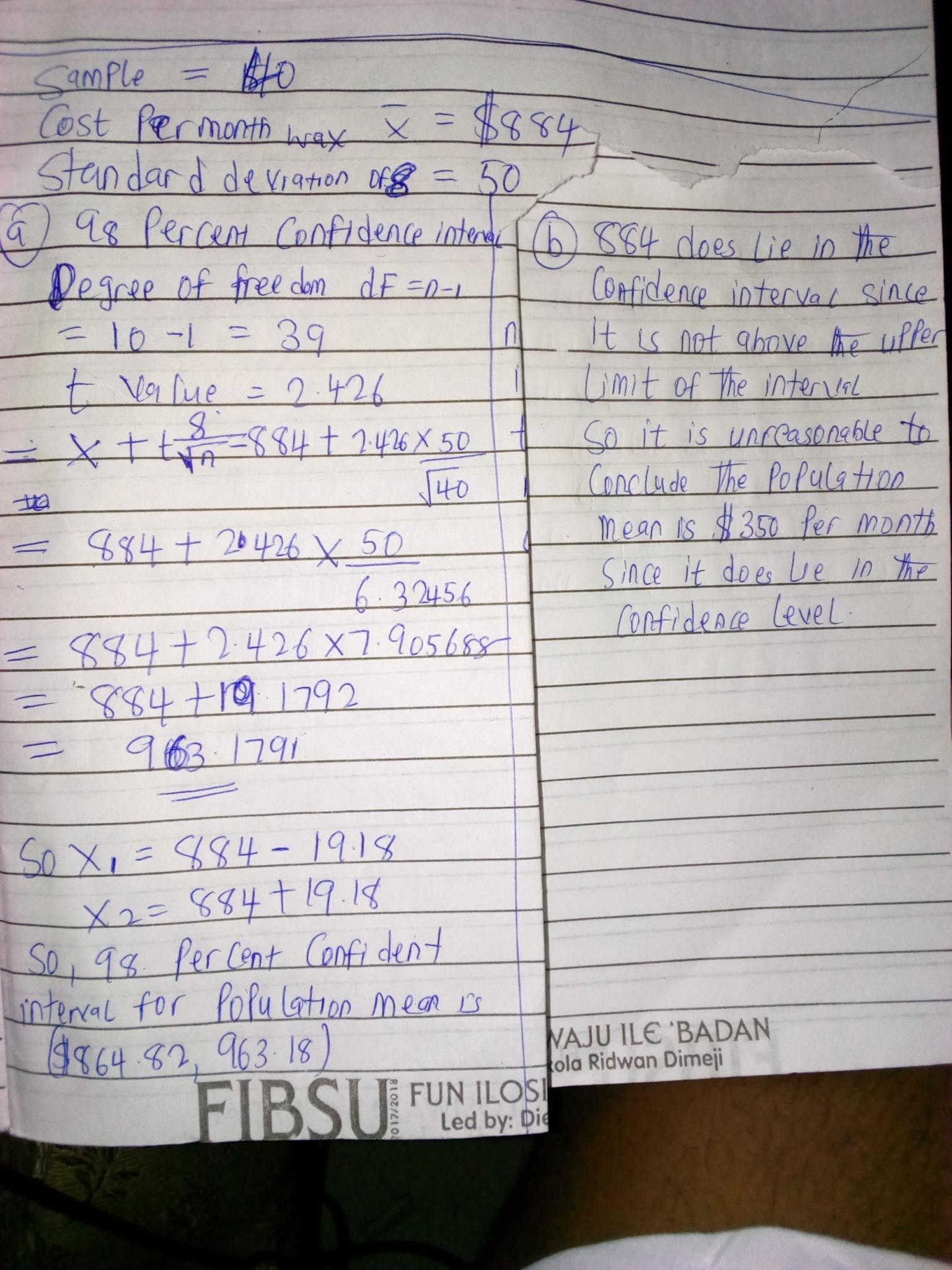

Answer:

1. X1=884-19.18

X2=884+19.18

2. It is unreasonable to conclude the population mean is $350

Explanation:

Kindly check the attached picture for detailed explanation and answer

Answer:

b. Suggestion 2

Explanation:

Suggestion 2 will increase the demand for public transportation because private transportation is a substitute. If it is expensier to use private transportation, some people that before used private transportation will start using the public one. Suggestion 1 and 3 will not increase demand (shift the demand curve in the demand and supply graph), they will result in changes in the quantity demanded (movements along the demand curve).