Answer:

Task a:

Single plant wide factory overhead rate = $13.75 per machine hour

Task b:

Assembly department = $15.50 per machine hour

Finishing department = $12.00 per machine hour

Task c:

Factory overhead allocated per unit:

Product A: $34.21

Product B: $10.40

Task d:

Multiple overhead absorption rate is better.

Explanation:

<h2>Task a:</h2>

For Task a, plant - wide factory overhead rate is required, which is blanket overhead absorption rate.

Blanket overhead absorption rate

- Single overhead absorption rate for the whole factory.

- Common absorption rate used throughout a factory and for all jobs and units of output irrespective of the departments in which they were produced or processed.

Formula

<em>Single plant-wide factory overhead rate = Total budgeted factory overhead cost ÷ Total expected machine hours</em>

Total budgeted factory overhead cost = $550,000

Total expected machine hours = 20,000 hours + 20,000 hours

Total expected machine hours = 40,000

<em>Single plant-wide factory overhead rate = $550,000 ÷ 40,000 = $13.75 per machine hour</em>

<h2>

</h2><h2>

Task b:</h2>

Compute the production department factory overhead rates, assuming the multiple production department factory overhead rate method is used. Assembly Dept. $ per mh Finishing Dept. $ per mh

Solution:

Assembly department:

Overheads for assembly department = $310,000

Machine hours for assembly department for product A and B = 15,100 hours + 4,900 hours = 20,000 hours

Overhead absorption rate for assembly department = $310,000 ÷ 20,000 hours

Overhead absorption rate for assembly department = $15.50 per machine hour

Finishing department:

Overheads for finishing department = $240,000

Machine hours for finishing department for product A and product B = 9,000 hours + 11,000 hours = 20,000 hours

Overhead absorption rate for finishing department = $240,000 ÷ 20,000 hours

Overhead absorption rate for finishing department = $12.00 per machine hour

<h2>

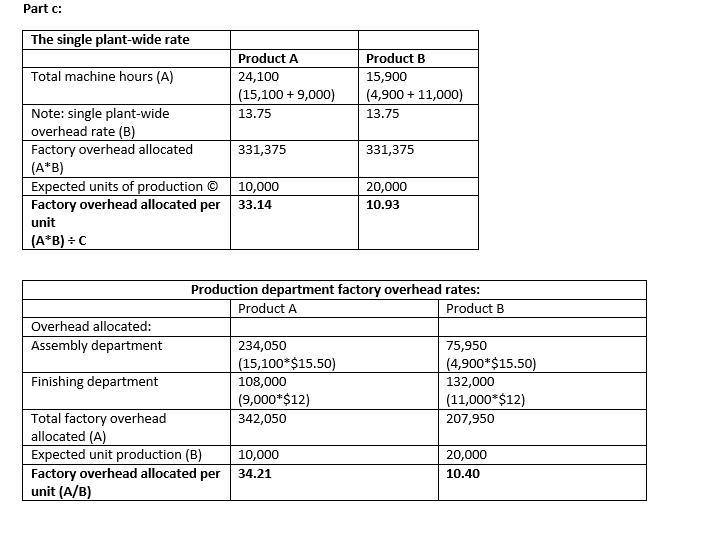

Task c:</h2>

Compute the factory overhead allocated per unit for each product using: The single plant- wide rate: Product A $ per unit Product B $ per unit Production department factory overhead rates: Product A $ per unit Product B $ per unit.

Solution:

Please see the attachment, as this is whole schedule for this task.

Factory overhead allocated per unit:

Product A: $34.21

Product B: $10.40

<h2>

Task d:</h2>

Which method is better (single or multiple)?

Single overhead absorption rate:

Plant or factory wide (single or blanket) rate is used for the whole factory and is assigned to all cost units irrespective of the departments in which they were produced.

<em>To use this method, there are certain conditions:</em>

- Company produces only one type of product.

- All production departments contribute in equal proportion to the fabrication of every product.

The above conditions restrict its usefulness and in the absence of above conditions. This does not produce satisfactory results.

Multiple/departmental overhead absorption rate:

In case of departmental overhead absorption rate, separate overhead absorption rates are used for different producing departments. Though use of departmental overhead absorption rate is considered better than using a single (factory wide) overhead absorption rate but it has certain pros and cons which are given below:

Advantages:

-

Use of separate rates for different departments facilities better control, as the departmental managers being responsible for costs of their respective departments have a closer look on overheads incurred.

- Per unit and total costs of a product can be more accurately.

Disadvantages:

-

This basis used for apportionment of overheads to different departments may not be fair or correct as overheads may not be incurred for the departments in the same way as shown by basis for apportionment.

- The departmental managers often do not have a significant role in the apportionment of overheads.

Therefore, multiple/departmental overheads is better to implement.