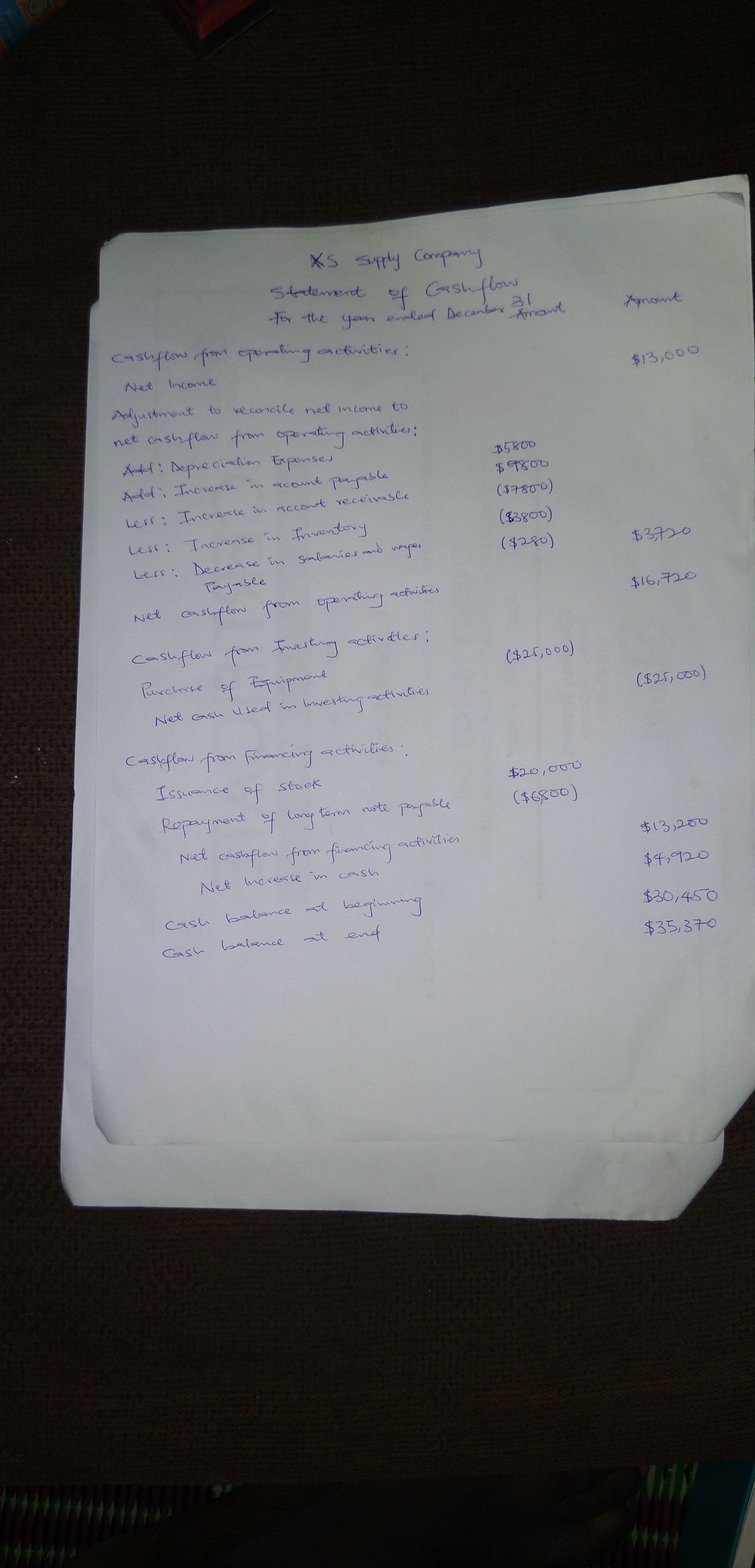

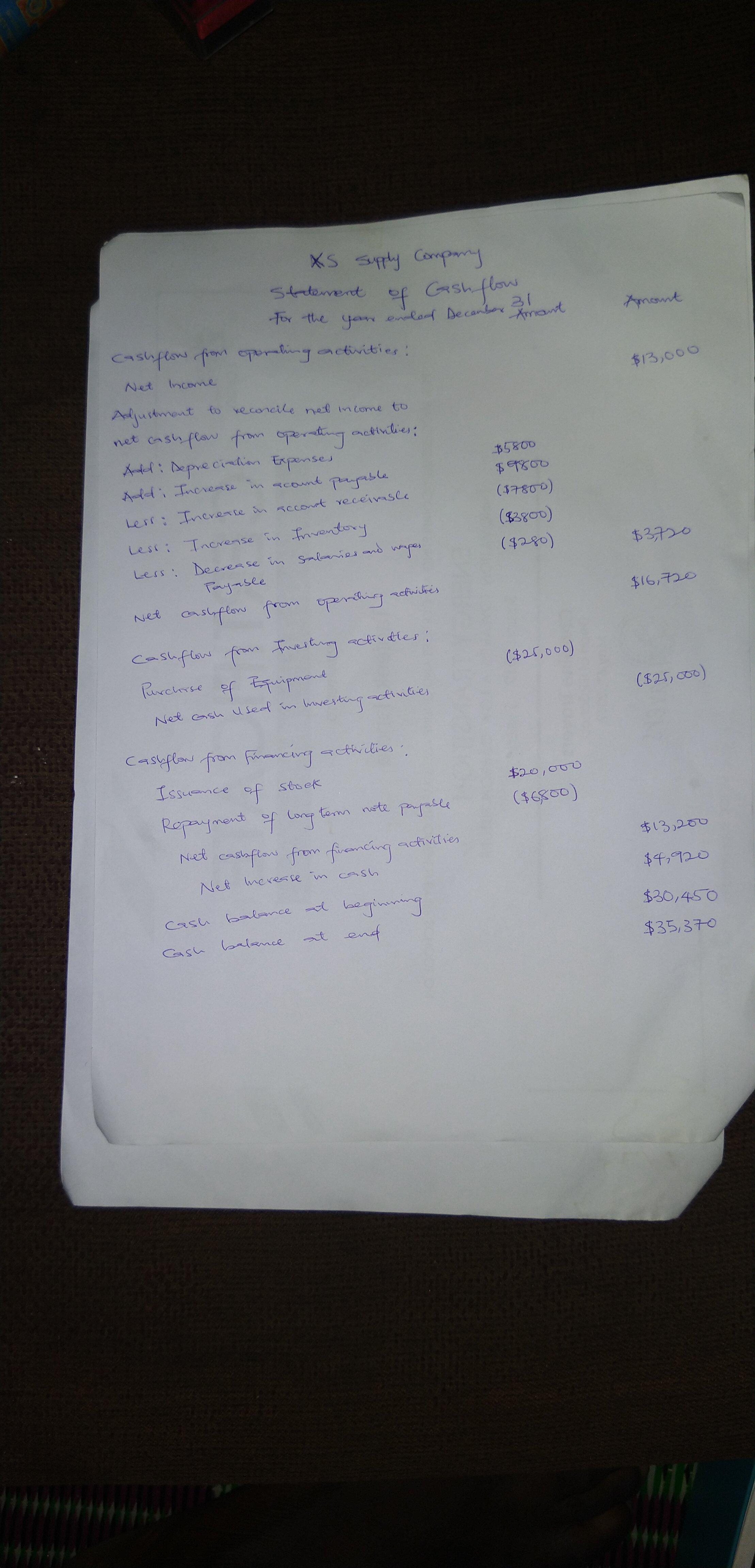

ment of cash flows. The completed comparative balance sheets and income statement are summarized:

Current Year Previous Year

Balance Sheet at December 31

Cash $ 35,370 $ 30,450

Accounts Receivable 36,600 28,800

Inventory 42,600 38,800

Equipment 133,000 108,000

Accumulated Depreciation—Equipment (31,600 ) (25,800 )

Total Assets $ 215,970 $ 180,250

Accounts Payable $ 37,600 $ 27,800

Salaries and Wages Payable 970 1,250

Note Payable (long-term) 45,200 52,000

Common Stock 93,400 73,400

Retained Earnings 38,800 25,800

Total Liabilities and Stockholders’ Equity $ 215,970 $ 180,250

Income Statement

Sales Revenue $ 128,000

Cost of Goods Sold 74,000

Other Expenses 41,000

Net Income $ 13,000

Additional Data:

a. Bought equipment for cash, $25,000. Paid $6,800 on the long-term note payable.

b. Issued new shares of stock for $20,000 cash.

c. No dividends were declared or paid.

Other expenses included depreciation, $5,800; salaries and wages, $20,800; taxes, $6,800; utilities, $7,600.

Accounts Payable includes only inventory purchases made on credit. Because there are no liability accounts relating to taxes or other expenses, assume that these expenses were fully paid in cash.

Required:

1. Prepare the statement of cash flows for the current year. Using the indirect method.

2. Evaluate the statement of the cash flows.