Answer:

Cost volume profit analysis (CVP) refers basically to determining the break-even point of a company and how we can use that information to predict how different changes might affect it. When you are performing a CVP analysis you have to decide which variables will be constant, i.e. ceteris paribus, and which will be altered to predict the effect on the company’s operating income.

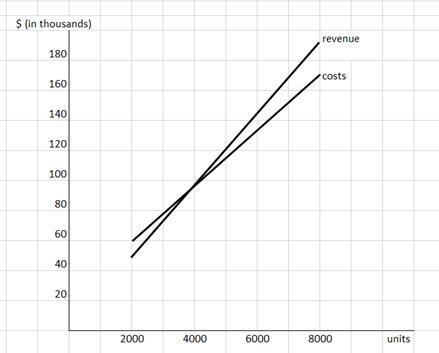

1)

sales level total revenue variable costs fixed costs total costs

2,000 48,000 36,000 24,000 60,000

4,000 96,000 72,000 24,000 96,000

6,000 144,000 108,000 24,000 132,000

8,000 192,000 144,000 24,000 168,000

2) break even point = 4,000 units