Answer:

The answers are Letters D and E.

Explanation:

The resulting report on the vulnerability scan should include some reference that the scan of the datacenter included 27 Win2003SE machines that should be scheduled for replacement and deactivation.

Remediation of all Win2003SE machines requires changes to configuration settings and compensating controls to be made through Microsoft Security Center's Win2003SE Advanced Configuration Toolkit.

What’s the quesitos asking? Like I know it’s a quick sort but like about what?

Answer:

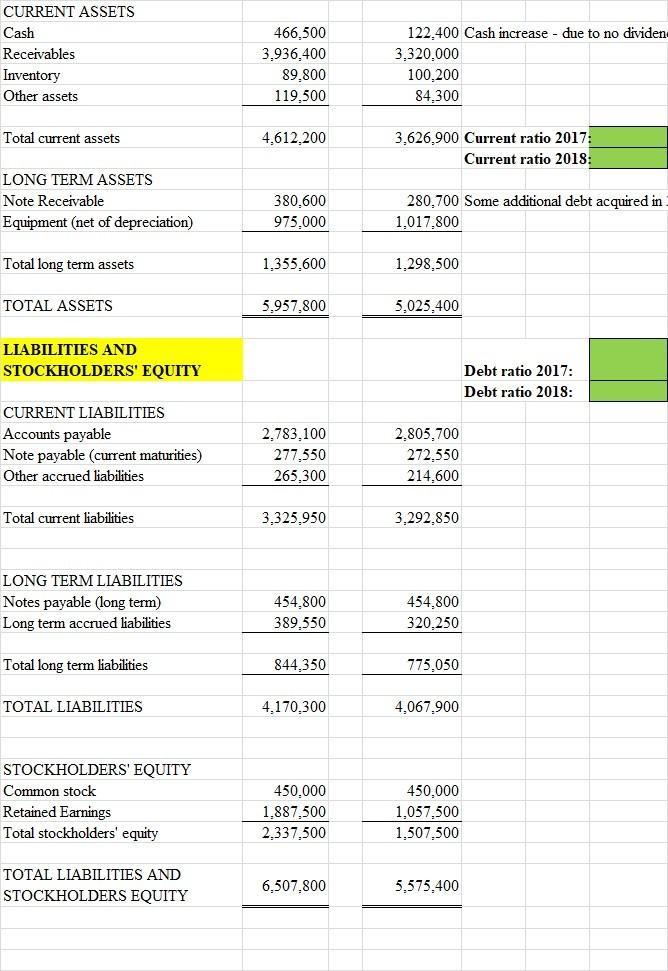

Gross profit margin requires revenue and gross profit of the company.

Current ratio = 1.386 x

Debt ratio = 0.123 x

Explanation:

Gross profit margin requires revenue and gross profit of the company which is provided in the question but it can be calculated using this formula ; Total revenue / gross profit . where Gross profit = Revenue - cost of goods sold

Current ratio is calculated using the formula ; current assets/ current liabilities lets assume the left column is for the most recent year then current ratio = 4612200/3325950 = 1.386x

Debt ratio is calculated using the formula ; total debts/total assets lets assume once more that the left column is the most recent year. note; total debts = long term + current notes payable = 454800 + 277550

therefore debt ratio = 732350 / 5957800 = 0.123x

attached is the income statement and balance sheet

Answer:

The correct answer is letter "C": Funds that arise out of normal business operations from its suppliers, employees, and the government, and they include immediate increases in accounts payable, accrued wages, and accrued taxes.

Explanation:

Spontaneous funds are all those incomes that a company receives without expecting them. The money can be received from different internal and external sources but they imply obligations. It means taxes are likely to be deducted after reporting the income in the firm's accounting books.