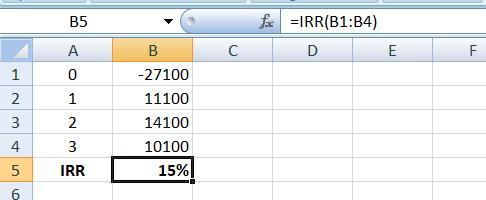

Answer:

15%

Explanation:

The computation of the internal rate of return is shown below:

Given that

Year Cash Flow

0 -$27,100

1 $11,100

2 $14,100

3 $10,100

The formula to compute IRR is

= IRR()

After applying the above formula, the internal rate of return is 15%

The answer to your question is,

civil rights infringement

-Mabel <3

Answer:

Price of the bond is $1,757

Explanation:

Coupon payment = 2000 x 6.4% = $128 annually

Number of periods = n = 20 years

Yield to maturity = 7.6% annually

Price of bond is the present value of future cash flows, to calculate Price of the bond use following formula

Price of the Bond = C x [ ( 1 - ( 1 + r )^-n ) / r ] + [ F / ( 1 + r )^n ]

Price of the Bond = $128 x [ ( 1 - ( 1 + 7.6% )^-20 ) / 7.6% ] + [ 2,000 / ( 1 + 7.6% )^20 ]

Price of the Bond = $128 x [ ( 1 - ( 1.076 )^-20 ) / 0.076 ] + [ 2,000 / ( 1.076 )^20 ]

Price of the Bond = $1295.03 + $462.15

Price of the Bond = $1,757.18

Answer: The correct answer is "3. platform project".

Explanation: This project is a platform project for Coolers Inc. because the change of voice sensors instead of remote controls or manual operations represents a change of platform for their products in which they have improved their technology.