A scene from a popular movie that shows an involuntary exchange (where a buyer or seller is forced to participate) could be in Star Wars, where it fictionally demonstrates the conquest of different planets and galaxies by force, through theft, destruction and violence.

If the exchange were voluntary, the negotiation would take place in a way that is beneficial to both the buyer and the seller, where each would be involved in a legal and ethical agreement to carry out a transaction.

<h3 /><h3>What is the benefit of voluntary exchange for the economy?</h3>

It assists in the positive development of the market, as voluntary exchange ensures that buyers and sellers benefit from an exchange process, which is an essential principle for the global free trade system.

Therefore, voluntary exchange must be promoted in the world economy, where nations exchange resources in ways that benefit local economic development.

Find out more about voluntary exchange here:

brainly.com/question/26349405

#SPJ1

<span>D is the correct answer. Discretionary funding is not essential for a person to live. Rent and groceries both provide basic human needs of shelter and food respectively, and deb repayment is necessary to avoid bailiffs. Vacations are an unecessary expense.</span>

Answer:

Mulch next to wood siding may lead to wood rot.

Explanation:

Based on the scenario being described within the question it can be said that Maura was noting this as a concern because Mulch next to wood siding may lead to wood rot. This mulch can hold moisture for extended periods of time which may cause the wood to rot. Once the wood rots it is too late and must be replaced which depending on the location of the wood can be extremely expensive.

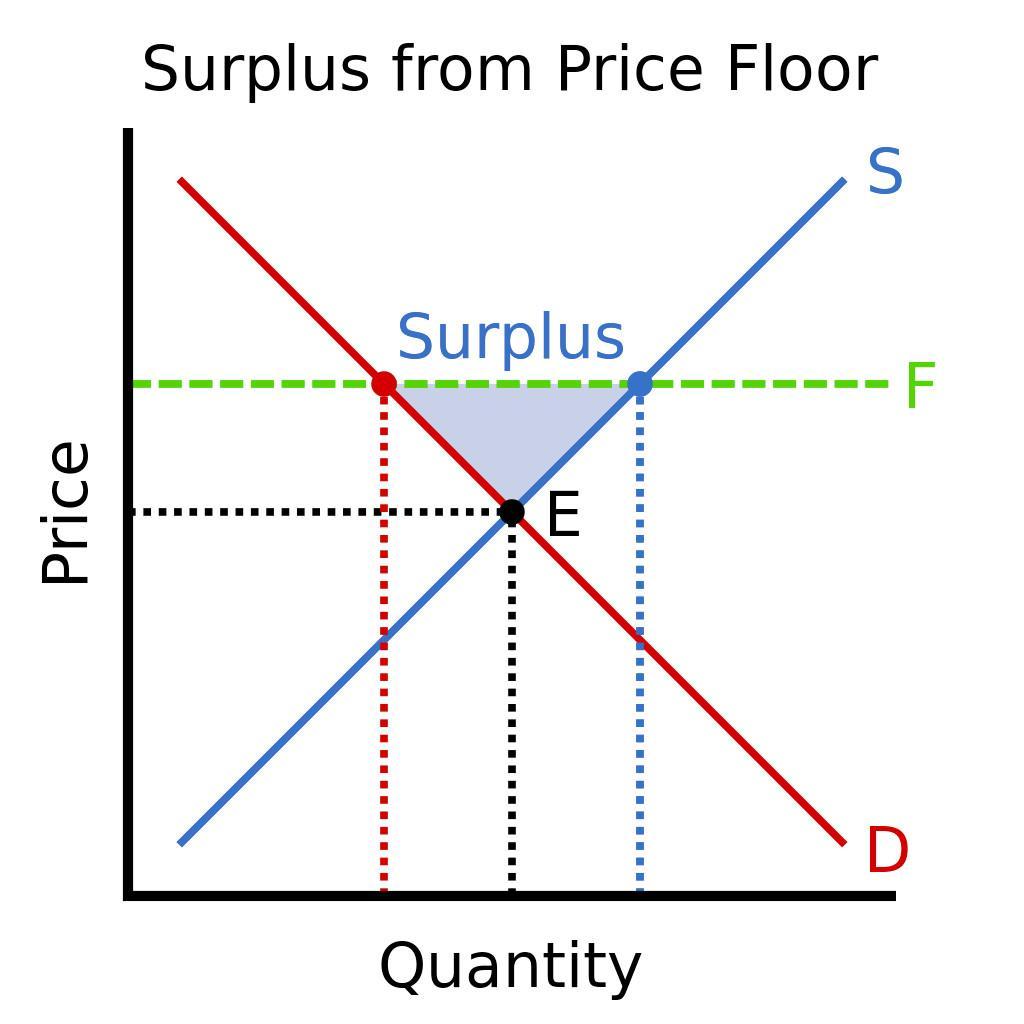

Answer:

B. The binding price floor will cause a surplus of wheat that farmers will be unable to sell.

Explanation:

A binding price floor is a minimum price that is above the equilibrium price.

Because the price is higher than equilibrium price, quantity supplied from farmers will be higher than quantity demanded from buyers, causing a surplus of wheat.