Answer:

The price of a one-year European put option on the stock with a strike price of $50 is $2.09

Explanation:

As, the call and the put option is of the same asset class, we apply call-put parity to find the price of the European put option.

The call-put parity function is:

C + PV(x) = P + S; in which:

C: Price of the call option = $6;

PV(x) : present value of strike price = Strike price in one year / e^6% = 50/e^6% = $47.09

P: price of the put option

S: spot price of the asset = $51

=> P = C + PV(x) - S = 6 + 47.09 - 51 = $2.09.

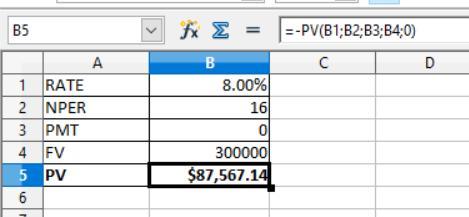

Answer:

$87,567.14

Explanation:

For computing the amount deposited for attaining the goal we need to apply the present value which is to be shown in the attachment

Provided that,

Future value = $300,000

Rate of interest = 8%

NPER = 16 years

PMT = $0

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the present value is $87,567.14

Answer:

establish a clear set of guidlines for employees to follow

Explanation:

Answer:

$21,800

Explanation:

The computation of 4-year revenue is as shown below:-

Bond Income of 4th Year = Face amount × Bond × 1 ÷ 2

= $500,000 × 8% × 1 ÷ 2

= $20,000

Interest Revenue = Bond Income + Amount of Discount Amortized

= $20,000 + $1,800

= $21,800

Therefore for computing the interest revenue we simply bond income with the amount of discount amortized.