Answer:

Explanation:

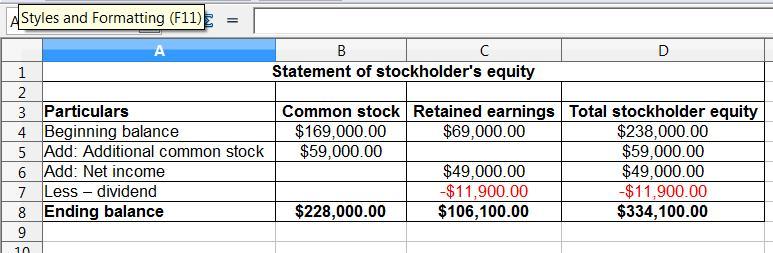

The statement of stockholder's equity comprises common stock and retained earnings. The ending balance after adjustment shown in the attached spreadsheet.

And, the balance sheet comprises of the assets and liabilities. With the help of the accounting equation, the total assets are equal to the total liabilities including stockholder's equity.

The preparation of the statement of stockholders’ equity and the balance sheet is presented in the spreadsheet. Kindly find the attachment below:

Answer:

A...increase

B...be unchanged

C....increase

Explanation:

It should be understood that it is only the telephone lines that was increased and not the number of the customer representatives, and also the number of the time they were using to attend to each customer was not reduced. So in this case, the number of customers that will be experience delay will definitely increase, why the time spent on phone by the customer representatives will remained unchanged, and the customer representatives utilization will increase too.

The approach to management Petra uses is called Flexibility.

Flexibility means adapting to situations as they arise. In management, it means management's ability to change approach to situations regarding their work environment.

Flexibility is important to management because it enables organizations address diverse employee needs. Also, Managers need to adapt to day-to-day shifts in workplace schedules – employee personal issues, an unexpected influx of work and more etc.

It therefore means that Petra is using approach to management called flexibility, which enable her change management style based on the reaction of her employees to a project.

learn more at : brainly.com/question/4971786

Answer:

B. 29.2%, 12.5%, 10.0%

Explanation:

Gross Profit = Sales - Cost of goods sold / Sales

Gross Profit = $1,200 - $850 / $1,200

Gross Profit = $350 / $1,200

Gross Profit = 0.2917

Gross Profit = 29.17%

Operating profit = Sales - Cost of goods sold - Operating Expenses / Sales

Operating profit = $1,200 - $850 - $200 / $1,200

Operating profit = $150 / $1,200

Operating profit = 0.125

Operating profit = 12.5%

Net profit margin = Sales - Cost of goods sold - Income Taxes / Sales

Net profit margin= $1,200 - $850 - $200 - $30 / $1,200

Net profit margin $120 / $1,200

Net profit margin= 0.1

Net profit margin= 10%