Answer:

D)the second-period demand curve will shift substantially to the right.

Explanation:

If monopolist succeeds in selling a sufficiently high quantity in the first period, then in the second period it will further increase and will shift the demand curve to right hand.

Answer:

False .It is called budget

Explanation:

Budget is used to estimate total costs of the project and it includes a detailed estimate of all costs that are likely to be incurred before the project is completed.

This is used for resource planning and control at every stage of the project and if there is any deviation ,this must be clearly justified by the project manager.

Answer:

see below

Explanation:

India has the longest coastline connecting it to Europe, Asia, and African countries. The coastline has helped India establish close contacts with these counties, which has benefited India socially, diplomatically, and economically.

some of the benefits include

1) Trade - The coastline allows India to trade with many countries due to its ease of accessibility. Importing and exporting to India is less expensive due to its proximity to the ocean.

2) Boast to tourism - a long coastline serves as a tourist destination.

3) Fishing- The coastline is a big opportunity for the Indian fishing industry.

4) Agriculture -The ocean influences monsoon rainfall to Indian, enabling it to profit from agricultural activities.

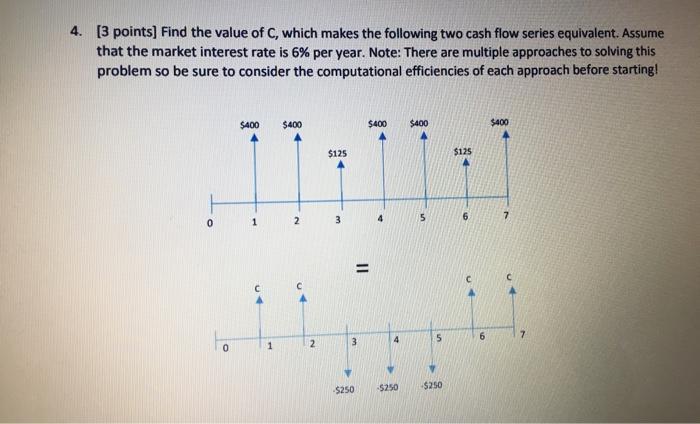

Answer:

Find attached complete question.

$ 750.10

Explanation:

In order to ascertain the value of C ,we need to equate the present value of the two streams of cash flows to each other as follows:

first stream:

$400/(1+6%)^1+$400/(1+6%)^2+$125/(1+6%)^3+$400/(1+6%)^4+$400/(1+6%)^5+$125/(1+6%)^6+$400/(1+6%)^7=$1,808.19

Second stream:

C/(1+6%)^1+C/(1+6%)^2-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5+C/(1+6%)^6+C/(1+6%)^7

-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5=-$594.74

C/(1+6%)^1+C/(1+6%)^2+C/(1+6%)^6+C/(1+6%)^7=C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651

simplification

C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651=C/(0.9434+0.8900+0.7050+0.6651)= 0.31216C

All in all:

$1,808.19 =-$594.74+ 0.31216C

$1,808.19+$594.74= 0.31216C

$2402.93

= 0.31216C

C=$2402.93* 0.31216 =$ 750.10

A public opinion is defined as an individual's opinions or experiences about a particular topic.