The correct entry to record the transaction concerning the company's sale of 10,000 shares of previously authorized stock is <u>a debit to Cash of $100,000 and a credit to Common Stock $100,000</u>.

<h3>Data Analysis:</h3>

Number of shares sold = 10,000

Par value =$10 per share

Cash $100,000 Common Stock $100,000

Thus, the correct entry to record this stock sale is <u>a debit to Cash of $100,000 and a credit to Common Stock $100,000</u>.

Learn more about recording the issuance of stock here: brainly.com/question/25562729

Answer:

Profit is higher, and output level is lower in Cournot.

Explanation:

Cournot competition is a type of economic model which describes an industry setting whereby firms that produce the same product compete on the amount of product to manufacture.

This type of competition involves more than one firm in which each firm's output decision affects the price of the product in the market. In cournot equilibrum each firm decide on the quantity of products to produce inorder to maximise profit.

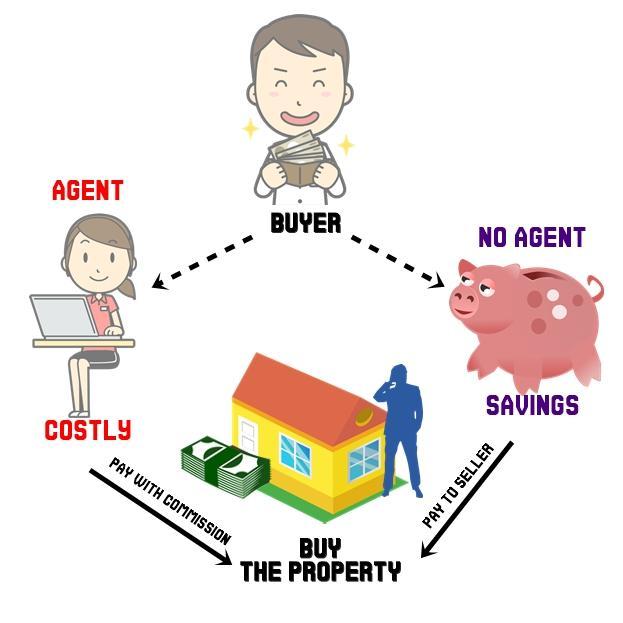

"The use of a buyer's agent guarantees that the buyer will get a property for the lowest price possible" is NOT an advantage of buyer's agency.

It is true that the efforts that a buyer's agent exerts on behalf of the buyer cannot be compromised and that the buyers can freely communicate confidential information without fear that disclosing that information will weaken their negotiating position. The buyers will also have the benefit of a licensee's expertise in finding the right property, negotiating the purchase and attending to closing details.

However, using a buyer's agent won't guarantee that the buyer can get the best deal on a property; as a result, this is not one of the advantages of buyer's agency. The agent would only consider what is best for the buyer and not the cheapest.

Agents will also charge extra fees and commissions for representing their buyers. To avoid additional expenses, some buyers and sellers choose not to use an agent. In order to save more money and find a property for the lowest price, buyers should avoid using an agent and instead deal directly with the seller.

Learn what happens when there's no buyer agency agreement in place here: brainly.com/question/28066390

#SPJ4

Answer:

The unstated assumptions in the problems given is that the company may require more units of aluminium and steel, which would allow for producing more bicycles.A linear programming model cannot account for this.

Explanation:

Linear programming model: this is an algebraic description of te objectives to be minimized and the constraints to be satisfied by the variables.

A tenant remains in possession of the leased property after the expiration of the lease term, without paying rent and without the landlord's consent, the tenant's status is Holdover Tenancy

This is further explained below.

<h3>What is

Holdover Tenancy?</h3>

Generally, A holdover tenant is a renter who continues to occupy a rental property after their original lease has expired but does not sign a new lease for the space.

In conclusion, Holdover tenancy refers to the situation in which a tenant continues to occupy a rented property after the original lease period has ended

despite the fact that the renter is not responsible for paying rent and does not have the permission of the landlord.

Read more about Holdover Tenancy

brainly.com/question/14366998

#SPJ1