Answer:

C. $50,000

Explanation:

Under IFRS section IAS 36, an impairment loss results from an asset's carrying value being lower than its fair market value or value in use. In this case, the fair market value of the asset (the price at which it could be sold) is $300,000, while its value in use is $400,000 (discounted to present value). In order to calculate the impairment loss, we must use the highest, in this case the value in use.

Impairment loss = $450,000 (carrying value) - $400,000 (value in use) = $50,000

Answer:

C) Factoring

Explanation:

In factoring, the Companies shall sell the accounts receivables to Tobit Financing at a discounted rate when they are apprehensive about receiving the same from their debtors in time. Once received by Tobit Financing, it shall recover the dues from those accounts at the full rate. The difference shall be the earning of Tobit Financing. This may also be true when such Companies are in urgent need of cash and this option seems to be the most viable.

Answer:

b) Reduce potential dilution

c) Have no effect on interest costs

Explanation:

Since in the question it is mentioned that the corporation is offering its existing bondholders for paying 6 1/2% this matured at the same time just like the convertible bond.

So here if the proposal is completed so the impact would be reduction in the potential dilution also it would not have impact on the effect on the interest rate and the same is to be considered

Answer: $321,020

Explanation:

The cash flow is expected to grow at a rate of 8%.

This means that in the next year it will be 8% higher than the $297,241 it is in the current period.

= 297,241 * ( 1 + rate)

= 297,241 * ( 1 + 8%)

= $321,020

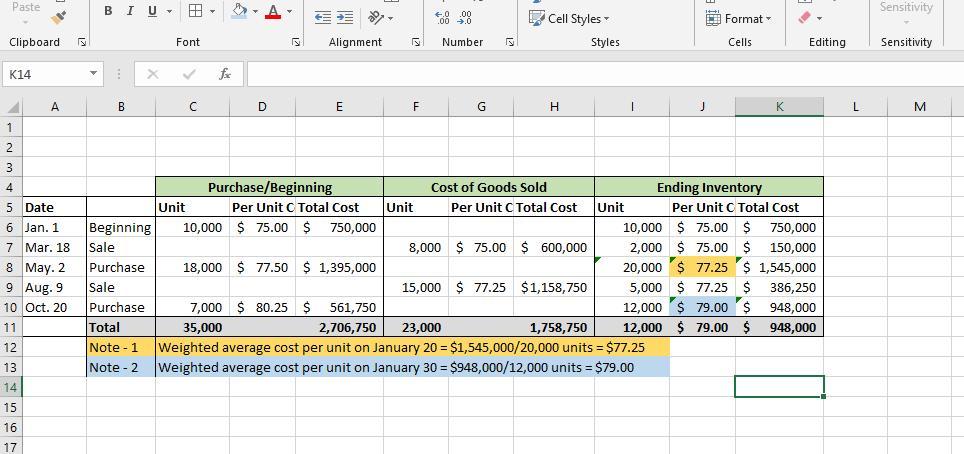

Answer:

See the explanation below

Explanation:

See the image below