Darnia is doing is called a <u>"dirty" </u>float.

A dirty float is a floating exchange rate where a nation's national bank infrequently intercedes to alter the course or the pace of progress of a nation's money esteem. In many occurrences, the national bank in a dirty float system goes about as a cradle against an outside monetary stun before its belongings wind up troublesome to the local economy. A dirty float is otherwise called a "managed float."

A dirty float system isn't viewed as a genuine skimming swapping scale in light of the fact that, hypothetically, genuine floating rate systems don't take into consideration intervention.

Answer:

d. Both a and b are correct.

Explanation:

Under a market economy the agents are free in both ways, they can arrenge their decision in open negociation with their supplier/employeer and can choose between the goods produced in the economy which ones to consume or not.

While in a communist economy it is a central planner who decide the output and payment for the families job.

Answer: insert anomaly

Explanation:

Based on the information given, since a single written record will have to be recorded as multiple sales records, this is an example of insert anomaly.

insertion anomaly simply means that the absence of other datas makes it unable for data to be added to the database.

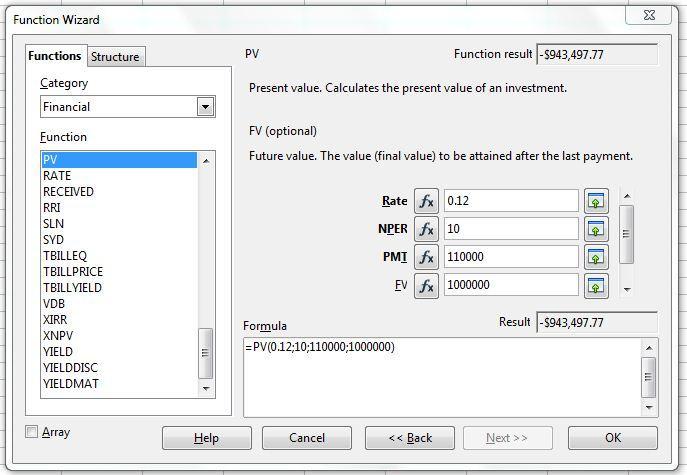

Answer:

Correct option is (c)

Explanation:

Given:

YTM (yield to maturity) (Rate) = 12%

Coupon rate = 11%

Face value = $1,000,000

Coupon payment (pmt) = 0.11 × 1,000,000 = $110,000

Time period (nper) = 10 years

Selling price of the bond is the present value of the bond which can be computed using spreadsheet function =PV(rate,nper,pmt,FV)

=PV(0.12,10,110000,1000000)

Present value of bond is $943,498 which is close to option (c)