Answer:

Direct material price variance

= (Standard price - Actual price) x Actual quantity purchased

= ($10 - $7) x 1,300 pounds

= $3,900(F)

Explanation:

Direct material price variance is the difference between standard price and actual price multiplied by actual quantity purchased.

(D) In order to prevent your account from going under zero you must remember what you spent your money on.

Nowadays you can check your bank accounts balance on your phone so you can see how much you spent.

Answer: B. Before purchasing a franchise, the buyer should carefully evaluate the franchise, the franchisor, his or her own situation, and the nature of the market

Explanation:

A franchise is a method that has to do with the distribution of products or services which involves a franchisor, and a franchisee. A franchisee pays a royalty an initial fee in order to do business using the name of the franchisor.

Before purchasing a franchise, the buyer should carefully evaluate the franchise, the franchisor, his or her own situation, and the nature of the market.

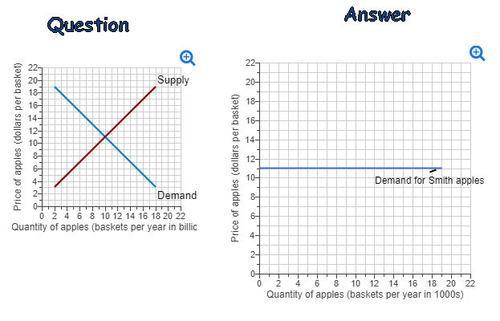

A perfectly competitive market is a market where there are many buyers and sellers of identical goods. The price of a good is determined by market forces. This means that price is determined at the intersection of the demand curve and supply curve for a good.

If a seller attempts to set the price for his good, the demand for his good will fall to zero as consumers would patronise other sellers who sell identical goods at a cheaper price. This means that the demand for goods in a perfectly competitive firm is perfectly elastic. Thus, the demand curve is horizontal.

Please find attached a graph that contains the answer. To learn more, please check: brainly.com/question/22698976

Squarespace would probably work. I use it as ecommerce store.