Answer:

$50,000

Explanation:

The theatre should record the securities at the date of donation for $50,000 because for donated securities, they are usually recorded at the fair value upon receipt. Also, for contribution - which is a gift, usually measured at the fair value when received to the not for profit organization , same applies to securities.

Answer:

a. Revenue - Income Statement

b. Common Stock - Balance Sheet

c. Current liabilities - Balance Sheet

d. Long-term Debt - Balance Sheet

e. Dividends - Statement of Shareholder Equity / Statement of Retained Earnings

f. Ending Cash Balance - Balance Sheet

g. Adjustment to reconcile net income to net cash provided by operations -Statement of Cash Flows

h. Cash spent to acquire the Buildings - Statement of Cash Flows

i. Income tax expense - Income Statement

j. Ending Balance of retained earnings - Statement of Shareholder Equity / Statement of Retained Earnings / Balance Sheet

k. Selling general and administrative expenses - Income Statement

l. Total Assets - Balance Sheet

m. Net Income - Income Statement / Statement of Shareholder Equity / Statement of Retained Earnings

n. Income tax payable - Balance Sheet

Joint intelligence planning supports joint operation planning and may result in the production of three products they are:

⇒Dynamic Threat Assessment

⇒Annex B: Intelligence

⇒National intelligence support plan

Joint operations are military actions carried out by joint forces and those Service forces employed in special command relationships with one another. Joint operations by themselves do not generate joint forces.

A joint force is a collection of assigned or attached components from important military departments that cooperate under a single joint force commander (JFC).

The Department of Defense (DOD) primarily employs two or more Services (from at least two Military Departments) in a single mission through joint operations.

To learn more about Joint intelligence here

brainly.com/question/14310090

#SPJ4

The correct answer is known as Flexible Premium Life Insurance.

Life Insurance or Insurance is described as an agreement among an insurer and a policyholder, wherein the insurer ensures promised payment of a death beneficiary to named beneficiaries upon the death of the insured individual. The Insurance Company creates an agreement upon a death benefit in consideration of the charge of premium with the aid of the insured.

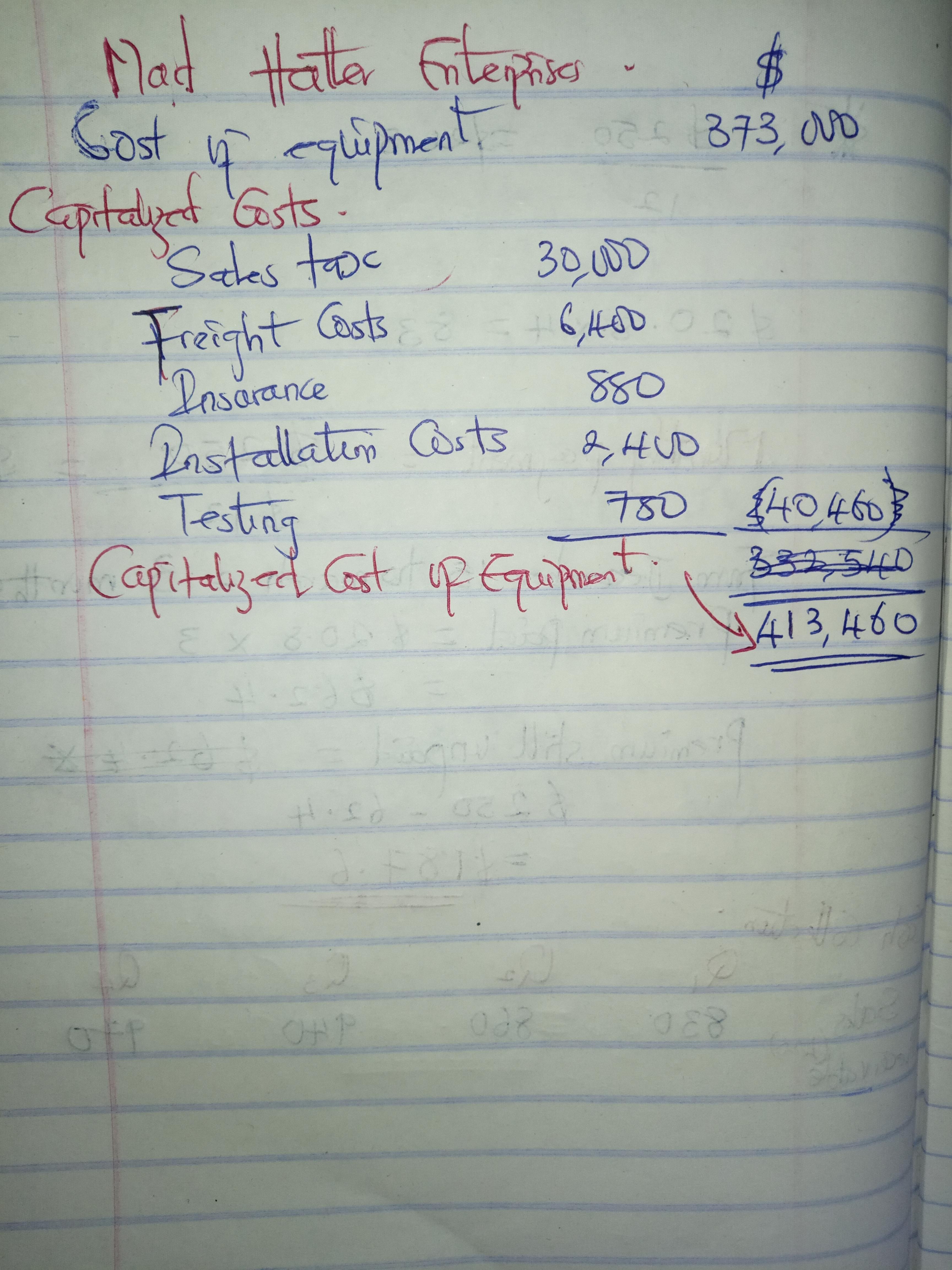

Answer: $332,540

Explanation: find attached my solution in the document below.

NB : note that the Insurance after equipment placed in service and Insurance for the first year of operations was not added because these are to be termed expenses to be deducted in the P & L account.