Even though I didn't see the video mentioned in the question, banks make most of their money through banking fees and investments.

Answer:

Need

Explanation:

Oil is a need for heating homes, running cars and factories + much more! It can be wasted by over-use, unnecessary usage and pollution

sorry for u

will they barn u

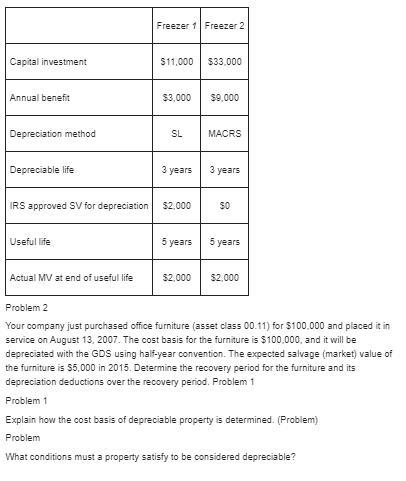

Freezer 2 is the better option because it has higher present worth.

I think 1 option is right answer