Answer:

<em>1. In this labor market, a minimum wage of $9.00 is binding : </em><em>FALSE</em>

<em>2. In the absence of price controls, a shortage puts upward pressure on wages until they rise to the equilibrium : </em><em>TRUE</em>

<em>3. If the minimum wage is set at $12.50, the market will not reach equilibrium : </em><em>TRUE</em>

<em>4. Binding minimum wages cause frictional unemployment : </em><em>FALSE</em>

Explanation:

<em><u>Question has been attached here</u></em>

Unemployment is the term used to define those who are willing and are actively seeking work but cannot find any. A minimum wage is a price control, in the form of a price floor imposed by government legislation in order to protect laborers from low wages. Paying anything below the minimum wage is against the law.

<em>1. In this labor market, a minimum wage of $9.00 is binding : </em><em>FALSE</em>

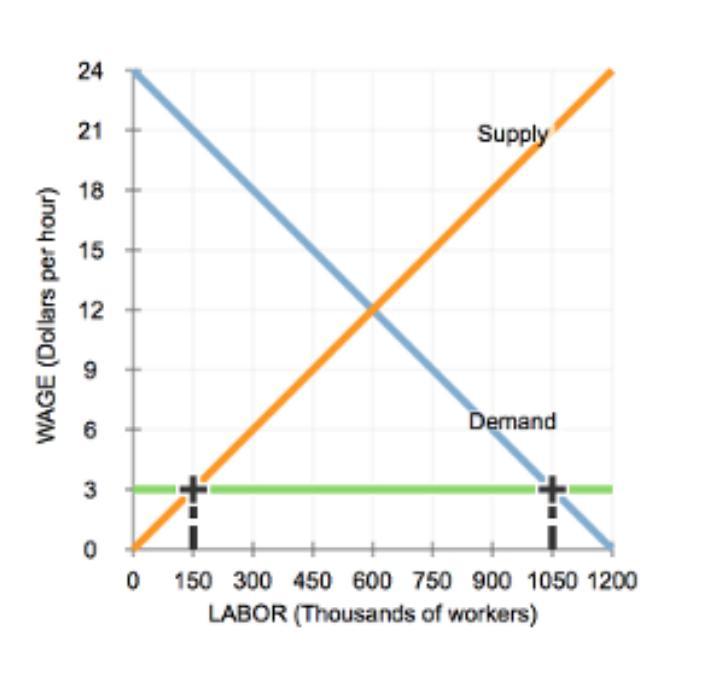

A minimum wage is binding only if it is set above the equilibrium price. In this scenario, the equilibrium price is at $12. Hence, $9 is not binding since a shortage of labor would gradually raise the price to the equilibrium.

<em>2. In the absence of price controls, a shortage puts upward pressure on wages until they rise to the equilibrium : </em><em>TRUE</em>

When there is a shortage in the market, it means that the quantity supplied is higher than the quantity demanded. With any particular commodity such as bread or rice, a shortage creates a rise in price. Just as that, a shortage of workers creates an upward pressure on the price (wage). Since there are no price ceilings, market will reach equilibrium.

<em>3. If the minimum wage is set at $12.50, the market will not reach equilibrium : </em><em>TRUE</em>

As shown in the diagram, the market equilibrium is $12. If the minimum wage was $12.50, there would be a surplus of labor (quantity supplied is higher than quantity demanded). Naturally, this may cause a downward pressure on wages until it reaches $12. However, when a minimum wage is imposed at $12.50, it cannot fall below that level. Thus, the market will not reach the equilibrium.

<em>4. Binding minimum wages cause frictional unemployment : </em><em>FALSE</em>

Frictional unemployment is a type of unemployment that occurs when workers are temporarily unemployed while switching between jobs. It is normal and occurs even in the healthiest of economies. A binding minimum wage is more likely to cause structural unemployment. This occurs when there is a mismatch between the skills of the labor force and the skills expected to be possessed by employers to do a particular job. Hence, even if jobs are available, the laborers are not suited to do them and thus are unemployed.