Answer:

B everyone's resources are limited

Explanation:

A trade-off will involve selecting one option from a variety of choices. In a trade-off, one has to forfeit one alternative to enjoy the other. A trade-off is the same as the opportunity cost. The cost of trade-off is expressed as the foregone benefit from the next best alternative.

A trade-off exists because people have to choose the best way to use their limited resources to satisfy unending needs. The few available resources, including time and money, cannot satisfy individuals' and households' needs and wants. People have to prioritize their needs and allocate resources accordingly. Both individuals and firms will often decide to cater to their most pressing needs first. By making those decisions, a trade-off is created.

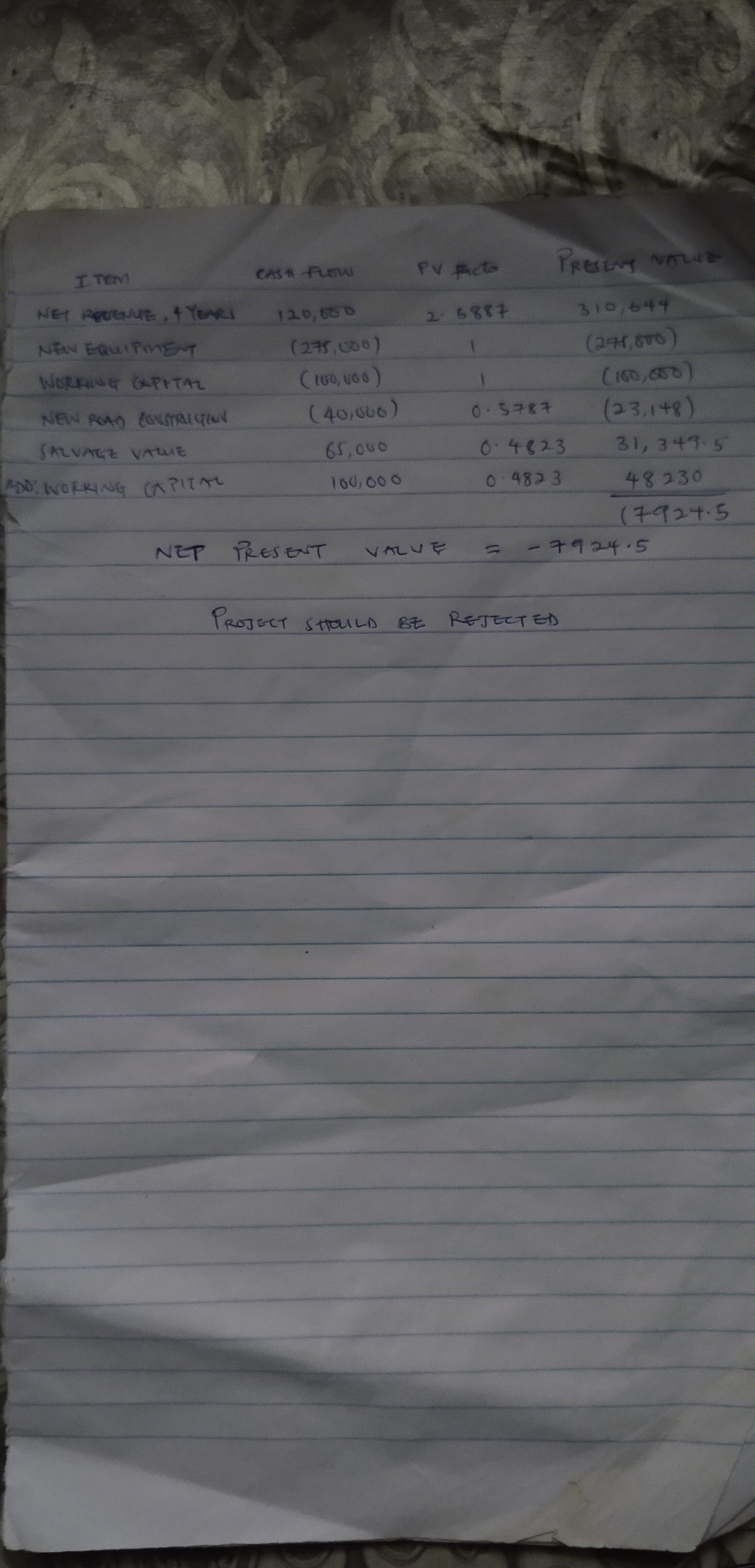

Answer: $7924. 5

Explanation:

Given the following :

Cost of new equipment and timbers - $275,000

Working capital required - $100,000

Annual net cash receipts - $120,000

Cost to construct new roads in year three - $40,000

Salvage value of equipment in four years - $65,000

Kindly check attached picture for Explanation

Answer:

$ 10512000

Explanation:

The market value of Madison investment which is the aggregate value of the company's investment =$ 12 million

The book value = assets - liabilities = (1700000 - 419000) ×0.4 = $ 51240

The year-end balance = $ 51240 + $ 10 million = $ 10512000 approx

Answer:

≈ 9644 quantity of card

Explanation:

given data:

n = 4 regions/areas

mean demand = 2300

standard deviation = 200

cost of card (c) = $0.5

selling price (p) = $3.75

salvage value of card ( v ) = $ 0

The optimal production quantity for the card can be calculated using this formula below

= <em>u</em> + z (0.8667 ) * б

= 9200 + 1.110926 * 400

≈ 9644 quantity of card

First we have to find <em>u</em>

u = n * mean demand

= 4 * 2300 = 9200

next we find the value of Z

Z = (  )

)

= ( 3.75 - 0.5 ) / 3.75 = 0.8667

Z( 0.8667 ) = 1.110926 ( using excel formula : NORMSINV (0.8667 )

next we find б

б = 200 = 400

= 400

Answer:

(B) Is the change in total cost from producing one additional unit of output

Explanation:

Marginal cost is the change in the total cost of production as a result of increasing the quantity produced by one unit.

Diminishing returns causes marginal cost to increase.

Marginal product of labor (MPL) is the change in output as a result of hiring one more unit of labour.