If the price of natural gas rises, the price elasticity of demand is likely to be the highest one year after the price increase.

<h3>What is the price elasticity of demand?</h3>

A measure of a product's consumption shift in response to a price change is called price elasticity of demand. The quantity shift in percentage terms divided by the price change in percentage terms is used to determine the price elasticity of demand.

The price elasticity of demand would probably be at its peak if the price of natural gas increased. Elasticity will be strongest in the long run since consumers would start exploring alternatives as a result of ongoing price increases.

Learn more about the elasticity of demand, here:

brainly.com/question/20630691

#SPJ1

Answer:

$720000

Explanation:

This answer is quite sole and can be obtained by simple addition.

The answer to this question can be gotten by adding the MACR property of 8byears that has a cost of $430,000 with the purchases of new machines whose cost is $290000.

= $430000 + $290000

= $720000

Therefore Maple's total MACRs deduction for the year 2020 is equal to

$720000.

Thank you!

Answer:

False

Explanation:

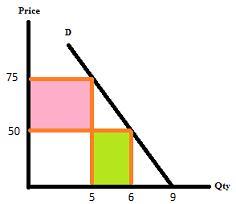

If Jake decides to increase total sales volume by decreasing the price of its engines, the decrease in price is too large compared to the increase in quantity demanded. The number of engines sold will increase from 5 to 6 (1 more unit) while the price of each engine will decrease from $75,000 to $50,000.

In this scenario, engines are price inelastic:

PED = % change in quantity demanded / % change in price = [(6 - 5) / 5] / [($50,000 - $75,000) / $75,000] = (1 / 5) / ($25,000 / $75,000) = 0.2 / 0.33 = 0.6

when PED is less than 1, the demand is inelastic. This means that a decrease in price will result in a smaller proportional increase in quantity demanded.

Answer:

The correct answer is "Continue producing 1000 units"

Explanation:

(In a perfect market)

When the price is = marginal cost. This means that if you increase your production, the benefits-profits will be the same as if you produce the same quantity.

When the Price > Marginal cost, means that consumers demand more for that good, so the producer has an incentive to increase the supply

When the Price < Marginal cost, means that production is higher than the consumer's demand. This is an incentive to decrease the supply.

For this case, the best option is to continue producing the same quantity of units, 1000 units

Answer:

Option C (perfectly elastic demand) seems to be the correct alternative.

Explanation:

- Large companies manufacture similar products which cannot be separated from those manufactured by certain rivals.

- Price increases become decided on the market as well as firm price changes, marketing their production at either the current market value. Increasing organizations face a relatively elastic consumer surplus equivalent to something like the sale value.

All other alternatives in question are not relevant to the unique scenario. But that's the correct answer above.