Answer:

Answer to the following question is as follows;

Explanation:

Several factors also influence the sort of planning application that must submit as well as the result of our planning permission.

Nature, animals, and biodiversity, as well as planning permission policies , Regulations, construction, and so on Statement of design, statement of design and accessibility, statement of design, statement of design, statement of design Environment Healthcare, Ecology

<span>Much of the methamphetamine consumed in the US is manufactured domestically by amateur chemists in meth labs from common household drugs and chemicals such as lye, lithium, and ammonia. Since the passage of the Combat Methamphetamine Epidemic Act of 2005, the Drug Enforcement Administration has reported a sharp decline in domestic meth lab seizures, but drug cartels continue to meet demand by manufacturing meth in Mexico and smuggling it across the border</span>

Answer:

C. Evaluate and motivate workers

Explanation:

This is the taks for middle mamagement.

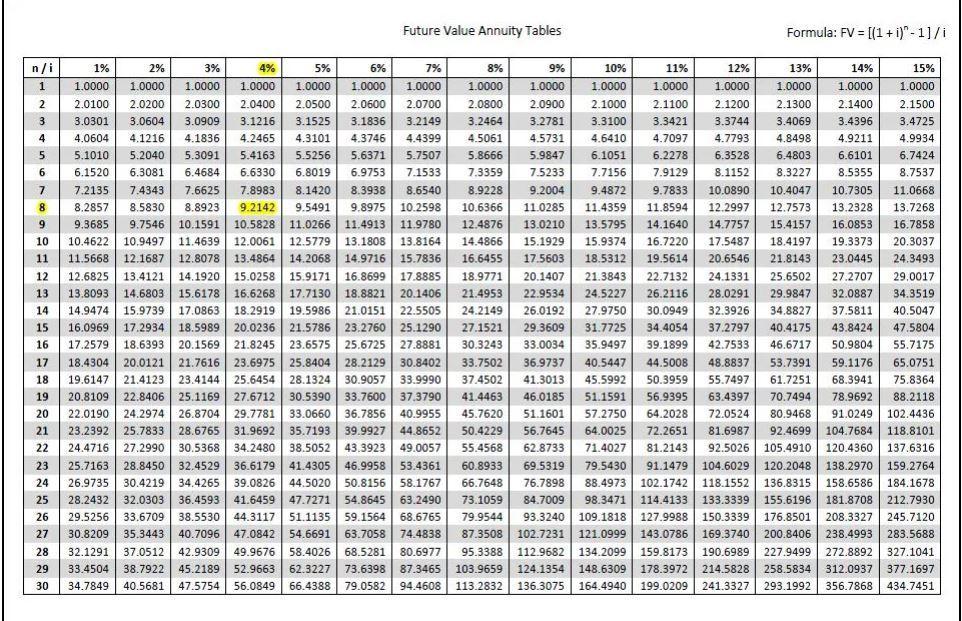

Answer: $3,153

Explanation:

The amount that will make you indifferent is the future value of the 3 payments at the end of those 3 years at 5%.

Future value of Annuity = Annuity * Future Value interest factor, 3 years, 5%

= 1,000 * 3.1525

= $3,153

Bank will require a final payment of $3,153 for you to be indifferent.

True......................................